by James A. Bacon

I am one of those schlubs who takes out insurance policies to protect against bad things happening. One eventuality I worry about is the need for long-term care. The longer you live and the more chronic conditions you develop, the greater the odds – about 50/50 for a 60-year-old today — that you’ll wind up bed-ridden at home or in a nursing facility. Feeling strong and fit at 53 when I took out a policy ten years ago, I was betting that I’d live longer than the average Joe and be more likely than not at some point in my life to benefit from having insurance. Signing up at a relatively young age would lock me in at an affordable rate. Or so I thought.

About two months ago I received a letter from my insurer, New York Life Insurance Company, informing me that my long-term care policy, which had remained stable ten years, was scheduled to increase 20%, costing me, in rough numbers, an extra $300 per year after a three-year phase-in. Three hundred bucks won’t bust the Bacon bank, but I was miffed — it was the principle of the thing. I had not been led to understand that my insurance rate would go up. And I bet there were other policy holders for whom $300 per year would cause real hardship.

Well, a look at my insurance policy indicated that, sure enough, New York Life was entitled to raise my fees. My bad. I should have read the fine print. Even so, any rate increase had to be approved by Virginia’s Bureau of Insurance, and I wondered — as I suppose an estimated 80,000 other long-term care insurance policy holders are wondering — what is the justification for jacking up our rates?

The letter referred vaguely to “longer life expectancies and an increased need for long-term care benefits.” Did the insurer mean to tell me that the people who are the world’s experts in demographic trends failed to anticipate that life expectancies would increase? And they miscalculated what percentage of the population would need long-term care? Really? That sounded lame to me, and I wondered if there was more to the story. In particular, I wondered if years of Quantitative Easing and low interest rates had depressed New York Life returns on insurance premiums below what the company had anticipated when it formulated the rates ten years ago. Could my higher insurance fee represent another $300 a year in tribute to Uncle Sam, just one of many ways in which low interest rates are invisibly transferring wealth from American citizens to its grotesquely swollen and indebted government?

One of the advantages of being a blogger is the ability to pick up the phone and call anyone with a decent chance that someone actually will answer. When I called New York Life to find out what the heck was going on, company spokesperson Terri Wolcott put me in touch with Aaron Ball, vice president and head of the Long Term Care business, who, as coincidence had it, lives in good ol’ Richmond, Va.

Low interest rates were a factor in the rate increases, Ball says, but not a decisive one. He candidly admits that the industry screwed up key underwriting assumptions.

We Underpriced the Policy. Sorry about That.

“When you apply for coverage, it can be 20, 30 or 40 years before you make a claim,” says Ball. “We set up reserves to pay claims 20 to 40 years in the future. We’re earning interest on those investments, and we assume what those interest rates will be.” Ten years ago, carriers were assuming earnings in the 5% to 6% range (conservative assumptions that were lower than what most pension funds were assuming at the time). “Today, they’re assuming in the 3% to 4% range. The low interest rates have put pressure on the portfolios.”

Higher returns on the company’s investment portfolios might have offset the negative experience, tempering the need for a rate increase, Ball says, but the bulk of the blame goes to actuarial miscalculations regarding other key variables.

Morbidity. The first the key variables is morbidity — how sick will policy holders get, and what will be the appropriate venue for treating them? When projecting 40 years into the future, getting this assumption correct can be harder than it looks. The things that put people into long-term care change over time. Ten years ago, frailty issues predominated — hip fractures, cardiovascular problems, and the like. Today, the driver is cognitive claims — Alzheimers and other forms of dementia. Also hard to predict is the setting in which people will be given long-term care. “Back in 1988, there was no such thing as an assisted living facility,” says Ball. As it turned out, New York Life’s morbidity assumptions were close to the mark. Other insurers got these assumptions wrong, and they’ve had to make upward adjustments in their premiums.

Voluntary lapse. When people buy policies, some continue to own the policy and eventually collect benefits, while others let their policies lapse voluntarily. The “lapsers” pay premiums that don’t get refunded, effectively underwriting the cost of the policy for others. When long-term insurance was getting off the ground about 20 years ago, there was no basis for determining how many policy holders would let their policies lapse, so carriers made the best guess they could. In most cases, those guesses were wrong.

New York Life assumed in pricing its premiums that policies would lapse at an annual rate of 2% after four years, but actual experience showed that the rate trended downward to about 0.5%. More people hung onto their long-term care insurance policies than the company expected.

Mortality. The rate at which policies lapse due to the policy holder’s death is another major variable. “We now expect twice as many people to be alive at age 90 compared to what was assumed when the product was priced,” says Wolcott. “Longer life expectancies generally result in additional claims because more people utilize long-term care services at older ages.”

The explanation made sense. I didn’t like it, but it made sense. New York Life blew two of its key assumptions (though not as badly as many other insurers did) and low interest rates depressed investment turns. Accordingly, to maintain the actuarial viability of the policies, the company had to jack up rates.

But the explanation raises a new set of questions. If policy holders sign a contract with an insurance carrier to provide a certain set of benefits for a certain price, why isn’t the carrier obligated to eat the difference when they make bad decisions? I’ve never heard of carriers filing to reduce premiums if their assumptions turn out to be too optimistic. Maybe it happens, but I haven’t heard of it. No, they keep the profit. Given the way the incentives are structured, aren’t insurance companies encouraged to low ball premiums, knowing that they can come back later and jack up rates?

So, Where Was the SCC?

Where was Virginia’s State Corporation Commission in all this?

Where was Virginia’s State Corporation Commission in all this?

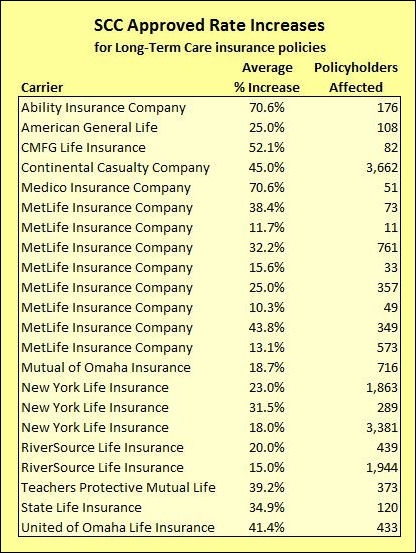

New York Life is hardly the only insurance carrier to ask for higher rates. The Bureau of Insurance has approved 22 rate increases by 12 different companies affecting nearly 16,000 policy holders. Another 35 requests affecting 65,000 policy holders are pending. Two companies are asking for 121% rate increases — more than double!

The Bureau has seen the problem coming for several years now. A March 2015 SCC order alludes to a 2012 report that noted the increase in the number and frequency of long-term care insurance premium rate increase requests. A 2013 report identified the lack of experience data, including changes in expected mortality, lapse rates and claim costs when the policies were formulated as driving factors behind the rate increases. “There would be no easy regulatory solution to this problem,” the report concluded, “and … any changes to the regulatory framework would require balancing multiple interests, including consumer protection and insurer solvency.”

Comments from 171 Virginia residents emphasized the “frustration and hardship felt by many long-term insurance policyholders… as well as their fears about the possibility of experiencing further rate increases in the future.” Policy holders felt it unfair that they would have to bear the burden of pricing errors made by the insurers, and they complained about the lack of transparency surrounding the rate increases and rate filings.

About thirty years ago, at the behest of the General Assembly, the Bureau of Insurance had adopted the National Association of Insurance Commissioners model legislation governing long-term care insurance. In 2000, Virginia adopted “rate stabilization” revisions to the rules that resulted in higher initial premiums and lower and less frequent subsequent rate increases.

The SCC’s 2015 order increases the consumer protections even more. Says SCC spokesman Ken Schrad: “At least 80 cents of each dollar in premium increase must be paid out in claims on an individual policy and 75 cents of each dollar in premium increase must be paid out in claims on a group policy.”

Wrote the SCC in that order: “While the Bureau’s proposed amendments to the Rules will not eliminate long-term care insurance premium rate increases, such proposed amendments adopt a more conservative approach for the initial pricing of long-term care policies, require insurers to take a more active role in managing long-term care insurance rates, and provide additional and necessary protections to long-term care insurance policyholders in Virginia.”

Bacon’s Bottom Line

I have no doubt that there is a delicate balancing act between protecting policy holders and ensuring insurers’ solvency. If you’re worried about policy holders getting the shaft, nothing could be worse than allowing a carrier to slip into insolvency unable to make good on any of its promises. I also recognize that regulators had no more experience than the carriers did when launching a brand new insurance product, so it was difficult to second-guess industry decisions. So, I’m mildly sympathetic to the position of the regulators, who have made appropriate adjustments over time.

However, it strikes me that something was severely askew with rules that resulted in insurance carriers in Virginia under-pricing 57 long-term care policies and, judging by the lack of any filing to lower rates, for zero to over-price them. I can assure you that the insurance agents selling these policies did not inform policy holders, “Gee, we’re really not very experienced at setting rates, and our assumptions could prove invalid, and if they do, we have the right to jack up your rights as much as we need to.”

The state of Virginia provides state tax credits for long-term care insurance premiums. The idea is to encourage Virginians to protect their retirement assets rather than fall back upon Medicaid to pay for their care. Some 80,000 Virginians went along, playing by the rules and doing the right thing. In the end, the insurance companies were protected from their mistakes, the federal government got rock-bottom interest rates that allowed it to continue running huge deficits while depressing insurance company portfolio returns, and thousands of Virginians got stuck with higher premiums. Their choice: either drop out and lose the money they have paid in, or suck it up and eat the new rate. Is there any wonder that Americans believe the system is rigged in favor of the powerful against the little guy?

Leave a Reply

You must be logged in to post a comment.