Hit the road, Jack

by Timothy Wise

Your humble scribe, ElGrowlerGrande, first became interested in the issue of taxation and interstate migration after reading a paper by Ohio University economics professor Richard Vedder. We discussed this in an article in the July 28, 2003 edition of The ACTA Watchdog, focusing on the question of how decisions of the Arlington County Board affect peoples’ decisions to move or stay.

Tables 1, 2, and 3 in that 2003 edition of The ACTA Watchdog, which used IRS county-to-county migration data, provided an array of information for tax years 2001-2002, and suggested a correlation between Arlington’s high taxes and peoples’ decision to move elsewhere.

Consequently, a series of posts the past week by Lyman Stone at the Tax Foundation’s Tax Policy blog caught our eye. Stone used a 5-part blog post to respond to a “voluminous” report, entitled “State Taxes Have a Negligible Impact on Americans’ Interstate Moves,” by Michael Mazerov of the very liberal Center on Budget and Policy Priorities (updated May 9, 2012).

Here is how Stone introduces the series, and summarizes what he consider’s the key claims in the CBPP study:

The Center on Budget and Policy Priorities’ Michael Mazerov has a voluminous new report discussing how state tax policies relate to migration. It’s an interesting debate to be had, both because migration is a major economic issue for many states, and because the two extremes of the debate tend to be so vocal. Advocates on one side appear to argue that small changes in taxes create huge changes in migration while advocates on the other seem to suggest that people don’t respond to taxes at all. CBPP’s new report says that “State taxes have a negligible impact on Americans’ interstate moves,” and so falls pretty comfortably in the “taxes don’t affect migration” camp.

The report’s key claims can be summarized as:

1. Interstate migration is small and declining, so, implicitly, it is not extremely economically important.

2. People mostly move for jobs, family, cost of living, and climate, but not for taxes.

3. Low- and middle-income households are more likely to move than high-income households, contrary to what “conservatives” claim.

4. High-tax states actually don’t have that much more net out-migration than low.”

Stone admits to there being “a grain of truth to CBPP’s position. People move for many reasons, and taxes are only one of many influential factors.”

The five parts in the series are too long to condense into even a medium-length Growls. Links to all five parts can be found here in part 5.

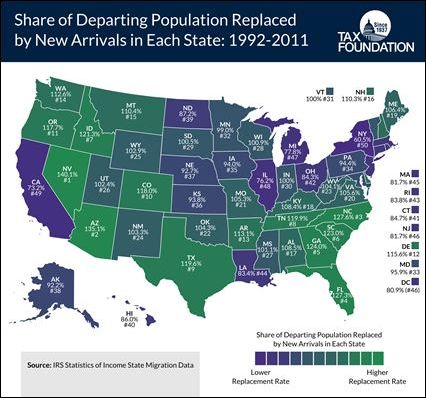

In part 5, Stone writes: “In a long series of tables and state-to-state comparisons, Mazerov lays out an argument that the migration flows between high-tax states and low-tax states are, contrary to public perception, actually quite similar. For example, he cites that 68.3 percent of the households moving out of New York will be replaced by households moving in, and offers a similar statistic for other states with net outward migration.” Stone then responds:

Unfortunately, he doesn’t provide the data for states with net inward migration. He also doesn’t provide information on how much income migrates; and in fact doesn’t even show the actual population changes, just the number of “households,” which may vary in size. These omissions are particularly odd as, in the paragraph right above the incomplete chart, he says it’s important to look at “all of the available migration data” (emphasis Mazerov’s). This could lead to readers getting the wrong idea that differences among state migration patterns are small. In fact, that is exactly what Mazerov does claim, when he says “As it turns out, net migration in most states is indeed quite small compared with total or gross migration” (emphasis Mazerov’s).

Stone also provides a table of the “differences in net migration” for the years 1992-2011. Just the differences for New York and Virginia are sufficient to show the significant differences in migration patterns between states:

- New York: 68.3% of departing households are replaced by new arrivals; 60.5% of departing population are replaced by new arrivals; and 59.9% of the departing income is replaced by arriving income.

- Virginia: 106.4% of departing households are replaced by new arrivals; 105.6% of departing population are replaced by new arrivals; and 101.6% of the departing income is replaced by arriving income.

Stone also presents the state data in the following Tax Foundation map:

Stone ends with the following summary:

On the whole, these high-inward migration states tend to have lower tax burdens. North Carolina and Idaho have periodically had higher than average tax burdens, but most, like Tennessee and Nevada, have consistently low tax burdens. Again, this doesn’t conclusively prove that taxes drive migration, as no doubt other living costs are lower in these states too: but it does suggest that taxes cannot be discounted out of hand.

In sum, we can’t conclusively say that lowering taxes will suddenly attract a tide of migrants. The connection between taxation and migration suggests that taxes affect migration on the margin, mostly impacting it through supporting economic growth and motivating upwardly mobile individuals. State policymakers are right to be concerned about migration in relation to taxes. But they should be careful to clearly explain that the main economic effect of better tax policy isn’t directly on migration, but on broader economic growth. Net inward migration is a positive side effect of economic growth and better tax policy (insofar as tax policy promotes growth), and shouldn’t be the fundamental goal of tax changes. (emphasis added)

Kudos to Lyman Stone and the Tax Foundation for helping American taxpayers to understand how and why taxes matter.

This piece was published orginally in the Growls blog by Timothy Wise under the pen name of ElGrowlerGrande.