Consumers account for roughly 70% of the U.S. economy, and their spending is the driving force behind economic growth. Over the past three business cycles, consumers increased their buying power through borrowing: running up credit cards, purchasing automobiles and houses on easier credit terms, and tapping their home equity. This trend was particularly pronounced during the Bush II expansion, a period in which incomes stagnated but consumers, buoyed by the rising value of their houses, borrowed more than ever.

Consumers account for roughly 70% of the U.S. economy, and their spending is the driving force behind economic growth. Over the past three business cycles, consumers increased their buying power through borrowing: running up credit cards, purchasing automobiles and houses on easier credit terms, and tapping their home equity. This trend was particularly pronounced during the Bush II expansion, a period in which incomes stagnated but consumers, buoyed by the rising value of their houses, borrowed more than ever.

In the United States, consumer debt grew from about 60% of GDP in 1990 to 96% of GDP by 2008, according to a McKinsey Global Institute report. A simple arithmetical calculation suggests that debt accumulation added an average of roughly 1.4% per year to economic growth over that period.

(For those generation war-mongers who would flagellate U.S. Baby Boomers for throwing prudence, frugality and thrift to the winds, it is worth noting that the leveraging of consumer debt was widespread throughout the U.S., Canada, Europe and South Korea as well. The debt accumulation coincided with a period of low and declining interest rates that reduced the cost of borrowing. McKinsey did not address why interest rates were so low, but the trend clearly seems connected to the “global capital glut” noted by Federal Reserve Chairman Ben Bernanke in a Sept. 11, 2009, speech to the German Bundesbank in Berlin.)

Not only will the U.S. economy lose the propellant of consumers getting into hock up to their eyeballs and spending with wild abandon, consumers will actually cut back their borrowing. In economist-speak, they will “de-leverage.” Although consumers have increased their saving in the past year or two (no mean accomplishment when joblessness and underemployment approach 18% of the workforce), they still have a lot of de-leveraging to go.

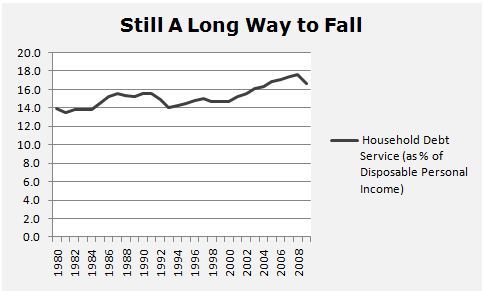

The chart to the left, based on Federal Reserve Board data, shows that service on mortgages, credit cards and other forms of household debt peaked at 17.5% of after-tax income in the third quarter of 2007 before falling to 16.4% two years later. That implies that consumers have accomplished only one-third of the de-leveraging needed to get back to the 14.0% indebtedness experienced as recently as 1993. (Click on image to view details.)

The chart to the left, based on Federal Reserve Board data, shows that service on mortgages, credit cards and other forms of household debt peaked at 17.5% of after-tax income in the third quarter of 2007 before falling to 16.4% two years later. That implies that consumers have accomplished only one-third of the de-leveraging needed to get back to the 14.0% indebtedness experienced as recently as 1993. (Click on image to view details.)

Economists debate whether the “new frugality” represents a fundamental shift in American values, or if consumers are just making a virtue of necessity as financial institutions curb their lending for their own reasons. Evidence suggests that a little of both is occurring. Boomers have awakened to the fact that they will retire soon and that they have done too little to prepare for life after the paycheck. Although some Boomers will put their faith in God or the U.S. government, others are trying to spend less and save more.

Similarly, there is evidence that the U.S. population generally has come to see the pitfalls in a life dedicated to the accumulation of material possessions and status symbols. As part of the nation’s greening consciousness, people are increasingly aware that buying more “stuff” sends economic and environmental ripple effects across the globe, from the decimation of rain forests to the emission of greenhouse gases. In a parallel trend, market research tells us that people are more likely to say that the most important priorities in life are friends and family rather than earning more money or being famous. It is unknowable how long this cultural shift will last, but when reinforced by badly burned financial institutions imposing stricter lending standards, it’s a good bet that consumer spending will remain depressed for years.

By simply not borrowing more, consumers will slow economic growth by 1.4% per year compared to the U.S.’s historic performance since 1990. If newly frugal consumers continue de-leveraging to levels of indebtedness prevailing 20 years ago, the unwinding could steal an additional 1.0% of annual economic growth over the next 20. Absent a new source of dynamism, a potential combined loss of 2.4% in the annual economic growth rate suggests that economic performance could be sickly for the next two decades.

So, how does this quick analysis inform our understanding of the debacle, known as Boomergeddon, to come? First, slow consumer growth must be viewed in the context of the massive overhang of bad commercial and residential real estate debt (see “The Ugly Ain’t Over Yet, Not by a Longshot” and “The Ugly Ain’t Over, Part II“), which will ravage bank balance sheets and crimp lending. If economic growth is slower and of shorter duration than projected by the Obama administration, deficits will be considerably higher than the $9 trillion between 2010 and 2020 also forecast by the Obama administration.

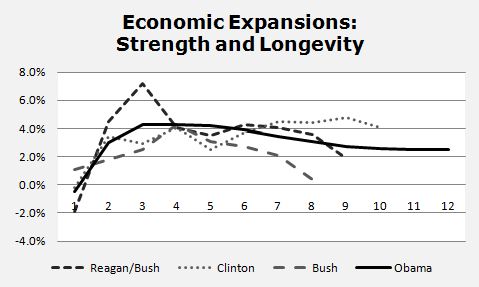

On the surface, the Team Obama’s 10-year budget forecast seems fairly cautious. This year, 2010, will resume economic growth at a tepid rate, but the expansion will gain momentum over the next few years and then settle into a slow-but-steady mode for the rest of the decade. However, a comparison with previous business cycles shows that the O Team is predicating its optimistic budget forecast on the strongest, longest economic cycle of the past 40 years. (Click on image to view details.)

On the surface, the Team Obama’s 10-year budget forecast seems fairly cautious. This year, 2010, will resume economic growth at a tepid rate, but the expansion will gain momentum over the next few years and then settle into a slow-but-steady mode for the rest of the decade. However, a comparison with previous business cycles shows that the O Team is predicating its optimistic budget forecast on the strongest, longest economic cycle of the past 40 years. (Click on image to view details.)

First, compare the Obama forecast for the first four years of the business cycle: Under an Obama presidency, the U.S. will outperform the first four years of the Clinton and Bush II business cycles, lagging only the turbo-charged expansion of the Reagan years. Moving into the middle years of the business cycle, Obama expects U.S. economic performance to trail Reagan and Clinton, but only by a modest margin. Then, in the final stages of the expansion, Obama expects the economy to keep to going — the Energizer Bunny of the economic world. While the Bush II’s business cycle lasted only eight years, Reagan/Bush’s nine and Clinton’s ten, Obama projects economic growth into the indefinite future in a state of never-ending bliss.

Needless to say, not everyone expects to see such a strong business cycle. Some, like U.S. Chamber of Commerce President Tom Donohue, have warned of a double-dip recession brought on by a wave of new taxes, regulations and mandates. One need not heed Donohue, however, to think that the current economic expansion will be weak — for reasons that predate Obama’s elevation to the presidency and have nothing to do with his political agenda. Let me emphasize: Republicans could win control of Congress this fall, Obama could lose re-election in 2012, a new team could enact a new economic policy, and the political pyrotechnics would not change the underlying economic trends. Obama’s sin is not in creating our current economic dilemma but in failing to acknowledge the effect it will have on the economy, deficits and the national debt over the decade ahead.

Boomergeddon is coming, baby. Deficits are gaining momentum, with entitlements and interest payments on the debt spinning out of control. Within a few years, the chain reaction will be unstoppable.