by Dick Hall-Sizemore

by Dick Hall-Sizemore

After more than a decade of state budget revenue shortfalls and concomitant budget cuts, one would think there would be smiles all round at the news of revenues coming in substantially above the projections, resulting in a healthy general fund surplus. Incongruously, that was not the case.

Republicans seemed to be outraged that the state brought in so much more money than was projected. There were calls to give it back to the taxpayers. It is somewhat curious that these are the folks who often demand that government be run like a business, yet there are no demands that large companies, such as big oil companies, for example, give refunds to their customers when they bring in record profits.

Governor Youngkin, not satisfied with large tax cuts in 2022, wants taxes cut even further. In July, citing the expectation of revenues exceeding the forecast (which was admittedly on the low side), he declared, “There’s no reason why we shouldn’t be able to have a substantial tax reduction.” In his address to the money committees in August, after citing the advances his administration had accomplished with the increased revenues and the challenges still ahead, he announced, “This is our moment to soar.” But, not too high, it would appear, because “we must provide substantial tax relief.”

Democrats, on the other hand, have been rather feckless. They resisted the Governor’s call for reductions in the top individual and corporate tax rates but went along with increases in the standard deduction and additional tax cuts for veterans. And, from the beginning, they advocated one-time tax rebates to individuals, eventually settling at $200 for individuals and $400 for those filing jointly. (It is an election year, after all.) It seemed that they were embarrassed over the good financial condition of the Commonwealth.

There are two situations that would justify tax cuts. The first would be a case of taxes being unreasonably high. The second would be a situation in which the government had sufficient revenue to meet the state’s needs and there was no responsible way to spend additional money.

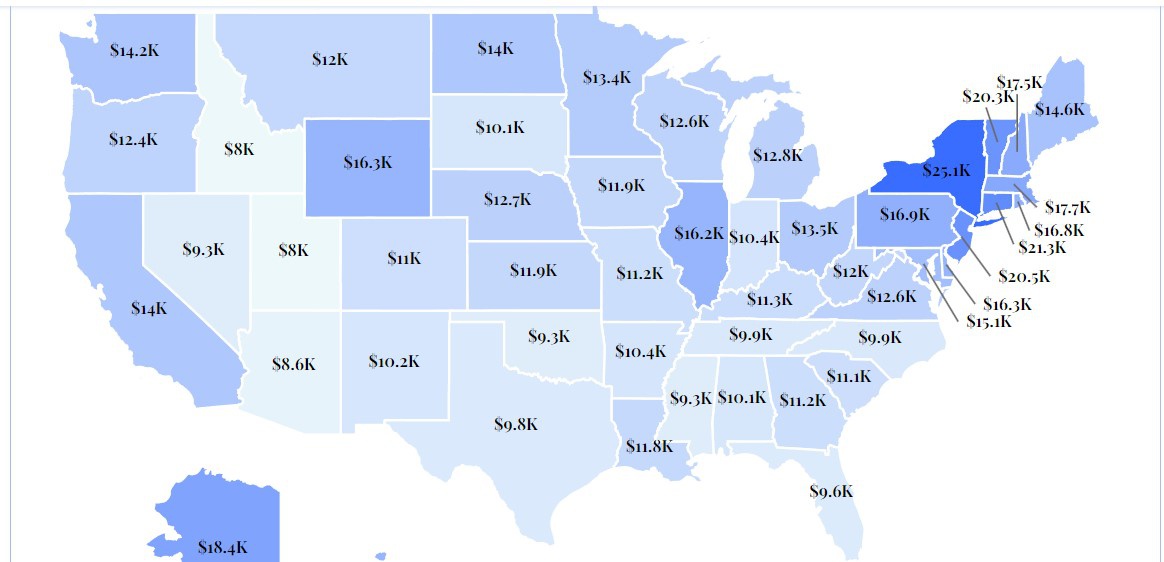

Let’s face it—no one likes to pay taxes. Furthermore, there are some that will always say that taxes are too high. However, despite the Governor’s claim that “the people of Virginia are overtaxed,” Virginia is not a high-tax state.

According to most analyses, the Commonwealth is ranked in the middle of all states in terms of the total state/local tax burden on individuals. For example, the Tax Policy Center, a joint enterprise of the Urban Institute and the Brookings Institution, ranks the Commonwealth no. 29 in percentage of personal income going to state and local tax revenues (the highest percentage is rank no. 1). The Tax Foundation ranks Virginia “26th overall in our 2023 State Business Tax Climate Index.”

As for unmet needs that would mitigate against tax cuts, is there anyone who can honestly say that there are no governmental activities for which additional funds are not needed? Consider the following areas:

K-12 Education

The Joint Legislative Audit and Review Commission (JLARC) has documented that the actual cost of implementing the state Standards of Quality (SOQ) is more than the cost calculated by the SOQ formula, upon which the state bases its SOQ appropriation. The localities pick up the balance. In FY 2021, JLARC calculated that, if the state had funded its share of the true SOQ costs, an additional $2 billion in state funds would have been needed. Furthermore, many educators contend that the SOQ standards are the minimum and additional staffing is needed.

Since FY 2021, the state has appropriated an additional $563 million in SOQ funding. Considering that the actual costs, and corresponding local spending, have increased, the gap between what the state’s appropriation is and what it should be is still quite large. Any additional tax cuts will diminish even further the ability to make up that difference.

Higher Education

Much has been written on this blog about the high cost of education and the burdens placed on students and parents. The Commonwealth has the opportunity to tackle that problem and need.

A major reason for this affordability problem has been the shifting of the costs of higher education from state appropriations to tuition. According to a 2022 study commissioned by the State Council of Higher Education for Virginia at the direction of the General Assembly, “The state’s institutions have grown rapidly more dependent on tuition revenue over the past two decades—the burdens of funding shifted toward students and families by 23.6 percentage points between FY 2000 and FY 2020, a greater change than in all but 10 other states.” Moreover, “comparison to institution-specific comparison groups of similar institutions across the country reveals that Virginia’s institutions collect more from tuition and less from state appropriations.”

Governor Northam and the General Assembly had taken some steps toward decreasing the dependence on tuition and fees. In the 2019 Session, the General Assembly provided an additional $52.5 million for FY 2020 to support higher education operations in exchange for institutions not increasing tuition. In subsequent years, additional appropriations have been provided to maintain or increase “affordable access.” These appropriations were placed in the “Education and General Programs” (E&G) accounts to be used for general operating expenses, the same as tuition and fee revenues. After FY 2020, there was no contingency regarding tuition increases. Since FY 2020, including the recently enacted budget, $490 million in new appropriations was provided over the course of the years. At the end of each biennium, the total of the second year appropriation was continued in the institutions’ base budgets. As a result, since FY 2020, higher ed institutions had been provided a total of $927 million to enable affordable access. At the end of this biennium, there will be $335 million in their base budgets to carry over into each year of the next biennium. A major infusion of additional funding of, say, $500 million next biennium ($250 million each year) could do much to further reduce the dependence on tuition.

Some readers of this blog will protest that giving higher ed such a large sum of money would validate its high costs and encourage growth in the administrative expenses, while tuition and fees would still be too high. Those would be valid criticisms. However, there are existing offsetting forces and additional steps that could be taken to improve the overall situation.

The Youngkin appointees now constitute a majority on all the boards of visitors. We can count on those appointees to begin reining in higher ed administrative expenses. Can’t we?

If such a large appropriation is provided to “maintain affordable access,” the Governor and the General Assembly could and should take further steps beyond just providing money. Each institution should be required to reduce its tuition and fees commensurate with the additional funding it received. For example, if an institution received $10 million out of that $250 million to maintain affordable access, it would have to reduce its tuition and fees by an amount that would have produced $10 million revenue. That would result in a net zero increase in E&G revenue. (Any additional increase in tuition and fees would be dependent on General Assembly approval.) Such a requirement would benefit all parents, but especially those middle-class parents whose kids did not qualify for need-based financial assistance.

To address the issue of bloated administrative costs, the Governor and the General Assembly could go further. They could require higher ed institutions to reduce their administrative costs by five percent and to reflect those savings in additional tuition and fee reductions. The best way to reduce an agency’s expenditures is to cut its budget and let it figure out the best way to absorb those cuts.

Mental Health

The need for more mental health beds in Virginia has been well-documented, as well as the need for more outpatient mental health treatment. To his credit, Governor Youngkin included in his budget proposals last winter a plan to build out a crisis response system for mental health. To the $78.3 million (some of it one-time funding) Youngkin included, the General Assembly added $68 million. To build out the crisis response teams; increase the capacity of the community services boards as recommended by JLARC; expand inpatient services; and support the findings and recommendations of the Virginia Behavioral Commission will require significant new funding.

Other

In addition to these three high-profile, high-cost areas, there are numerous needs in smaller areas that do not get much attention. Two examples would be (1) indigent defense in which there is a need for higher pay and additional staff; and (2) more Health Department inspectors for nursing homes, which Jim Sherlock has documented on this blog.

The 900 million dollar-question

The compromise reached by Republicans and Democrats over the state budget included an increase in the standard deduction, a tax cut for veterans, and one-time rebates of $200 for individuals and $400 for couples filing jointly. Citing the uncertainty of future revenues and not wanting to bake additional tax cuts into the Code, the Democrats had insisted on the rebates instead.

The following argument deals with the rebates only. It is estimated that they will total $906.8 million. A lot of those rebates, probably a large majority of them, will go to people who do not really need it.

Using the same conservative approach taken by the General Assembly, how could that $906.8 million have been put to a one-time use with a long-term benefit for the Commonwealth? There are several uses that could be proposed, but they would involve the creation of new programs or expansion of existing ones. However, there are two potential uses that, if implemented, would have reduced future costs:

Debt service savings

A lot of bonded indebtedness was authorized in recent years. The Department of the Treasury does not actually issue debt that has been authorized for a project until the agency anticipates using the cash. General fund appropriations could be substituted for debt for the balance of any remaining bond authorization for a project. The Secretary of Finance, in his capacity as chair of the Debt Capacity Advisory Committee, informed the Governor and clerks of the two houses of the General Assembly last fall that “there is currently [as of July 2023] $4.0 billion in previously authorized but yet to be issued tax-supported debt that is anticipated to be issued over the next four to five fiscal years.” Although Treasury has issued some more debt since then, it is reasonable to assume that there is still approximately $3 billion remaining in authorized, but unissued, tax-supported debt. Using that balance of $906 million to supplant that much unissued debt would have enabled the state to avoid debt service costs on that amount in the future and, with interest rates rising recently, the future savings could have been significant.

Unfunded VRS liability

The director of the Virginia Retirement Service reported to the Virginia House Appropriations Committee in January, 2023, that the retirement plan for state workers had an unfunded liability of $5 billion, while the unfunded liability retirement plan for teachers was approximately $11 billion. A one-time infusion of $906 billion would have significantly reduced future costs of maintaining the viability of the plans. For example, the report estimated that a $1 billion appropriation would result in savings of $2 billion over 20 years.

Unfortunately, rather than taking a long-term perspective, the General Assembly chose the equivalent of a temporary sugar high.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply

You must be logged in to post a comment.