by James A. Bacon

by James A. Bacon

The last time the United States had a serious conversation about deficit spending and the accumulating national debt was in 2010 with the publication of the Simpson-Bowles study. (That’s about the same time I wrote Boomergeddon, predicting that the United States had 20 to 30 years before the fiscal wheels fell off the bus.) After the usual tut-tutting, and Republicans blaming Democrats, and Democrats blaming Republicans, nothing was done. Indeed, in the following era of artificially low interest rates that made deficit spending seem painless, Congress, successive presidents, and the media ignored the issue and deficits ballooned.

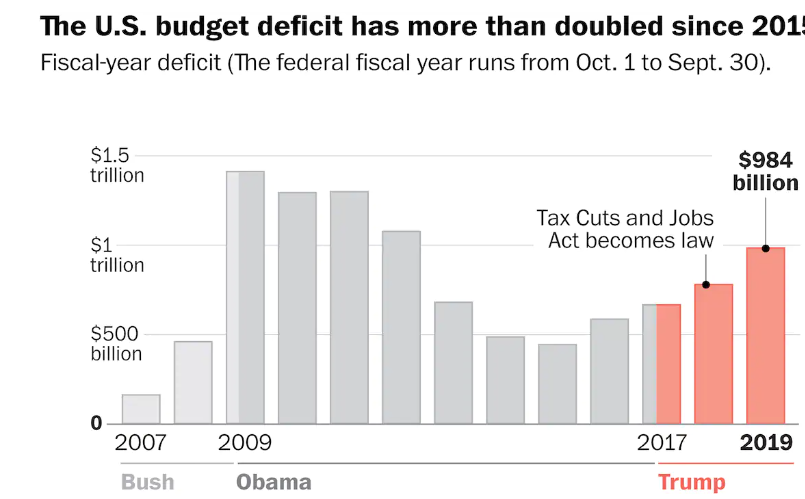

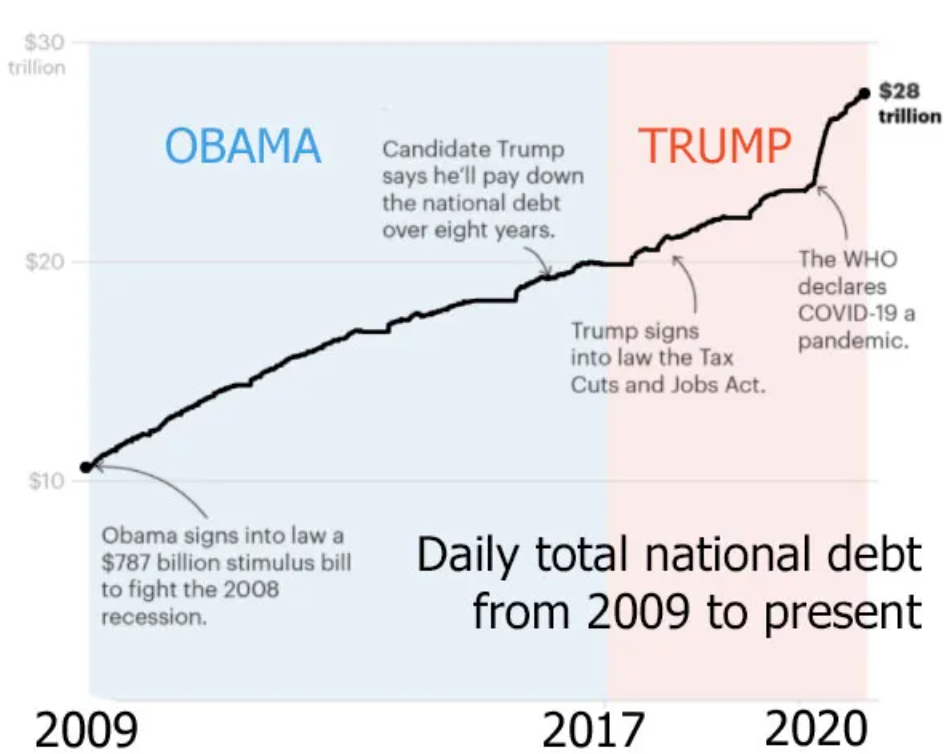

Now the national debt exceeds $34 trillion, the debt-to-GDP ratio exceeds 100%, the structural budget deficit is running between $1 trillion and $2 trillion annually, and it will be only a decade before the Social Security Trust fund runs out and sparks a fiscal/political crisis. Political polarization is even worse today than it was during the Obama presidency. Democrats and Republicans accuse one another of sabotaging democracy, and trust in our institutions has reached an all-time low. It’s as if the captain and the executive officer of the Titanic were fighting for control of the vessel, rolling on the deck trying to gouge each others’ eyes out, even as its prow dips below the icy waters.

Meanwhile, there is no cognizance in the political rhetoric here in Virginia of the fiscal perils to come. The Commonwealth is required by its state constitution to balance its budget, and the state has managed to retain its AAA bond rating, so we are not as wildly profligate as some other states. I suppose there will be some temporary comfort in the thought that we were not the first to plunge into ungovernable anarchy when the federal government fails. But that comfort likely won’t last long.

When fiscal collapse and/or hyper-inflation occur, responsibility for holding society together will fall to state and local governments. Virginians should start reining in spending now, bullet-proofing balance sheets, and identifying trouble spots not only in government finances but also in the multitude of quasi-governmental authorities we depend upon for government services. We should be preparing for the day, for instance, when the Metropolitan Washington Area Transit Authority (WMATA) goes bankrupt and the federal government has lost its capacity to continue subsidizing it.

I sound these gloomy notes because awareness of an impending fiscal cliff is back in the news, at least for the moment.

On last Sunday’s 60 Minutes Federal Reserve Board Chair Jerome Powell said the unthinkable: the nation’s fiscal policies are “unsustainable.”

SCOTT PELLEY: But is the national debt a danger to the economy in your review? You are this country’s central banker.

POWELL: So, it, I would say this. In the long run, the U.S. is on an unsustainable fiscal path. The U.S. federal government’s on an unsustainable fiscal path. And that just means that the debt is growing faster than the economy. So, it is unsustainable. I don’t think that’s at all controversial. And I think we know that we have to get back on a sustainable fiscal path. And I think you’re starting to hear now from people in the elected branches who can make that happen. It’s time that we got back to that focus.

I think the pandemic was a very special event, and it caused the government to really spend to ward off what looked like very severe downside risks. It’s probably time, or past time, to get back to an adult conversation among elected officials about getting the federal government back on a sustainable fiscal path.

PELLEY: I have the sense this worries you very much.

POWELL: Over the long run, of course it does. You know, we’re effectively — we’re borrowing from future generations. And every generation really should pay for the things that it, that it needs. It can cause the federal government to buy the things that it needs for it, but it really should pay for those things and not hand the bills to our children and grandchildren.

I think this is, again, not controversial. But it’s difficult from a political standpoint. It’s not our business, really. But I do think it’s pretty widely understood that it’s time for us to get back to putting a priority on fiscal sustainability. And sooner’s better than later.

PELLEY: Urgent?

POWELL: You could say that it was urgent, yes.

Then there’s this from Jamie Dimon, as Fox Business reports his words to the Bipartisan Policy Center:

Fed Chair Powell joins a number of critics of fiscal policy and the surging national debt, including JPMorgan Chase CEO Jamie Dimon. Dimon, warned last month that the U.S. economy is headed for a “cliff” if something isn’t done to address the federal government’s excessive debt burden.

“We see the cliff. It’s about 10 years out, we’re going 60 miles an hour [toward it],” he said at a Bipartisan Policy Center panel. Dimon argued that U.S. lawmakers will need to alter the current path of spending and control the national debt or there could be “rebellion” among foreign owners of U.S. government bonds.

The fiscal cliff is ten years off (right on schedule, if you go back and read “Boomergeddon.”) The welfare state erected over the past century is heading for a massive fail. Just imagine the turmoil if the federal government, unable to borrow to cover its spending, had to cut programs overnight by $2 trillion or, alternatively, if it paid for spending by goosing the money supply, not just one or two years as it did post-Covid, but year after year after year.

The nation’s political leadership is so dysfunctional, the increase of compounding interest payments on the national debt is so relentless, and the time left to fix things is so limited that catastrophic fiscal failure is mathematically ordained. State government is the only thing that stands between anarchy and order. But even in Virginia, most are in denial.

{kind=link}

{kind=link}

{kind=link}

Leave a Reply

You must be logged in to post a comment.