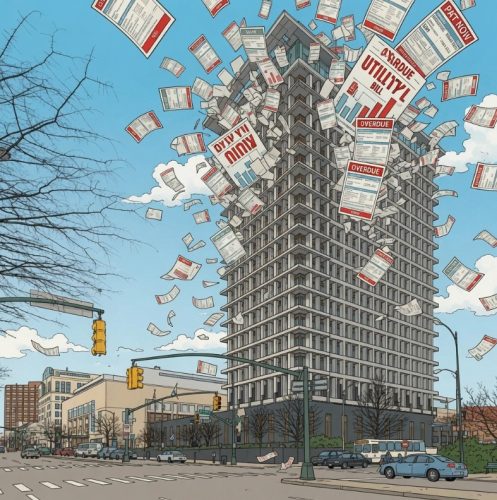

The biggest wave generated by the city’s Atlantic Park project is debt. The promised tax revenues aren’t sufficient yet to support it.

by James C. Sherlock

From an article by Stacy Parker in The Virginian-Pilot this morning:

To build two parking garages and improve streets in Atlantic Park, a public entity borrowed $53 million and agreed to pay off the loan with tax revenue generated from the project.

The bill has come due, but the taxes aren’t adding up yet.

Who knew?

About that $53 million debt thing. The Official Statement prepared by the City of Virginia Beach, Virginia, on behalf of the City of Virginia Beach Development Authority (the “public entity” referenced by Ms. Parker) listed the debt:

City Of Virginia Beach Development Authority

- $33,435,000 Public Facility Revenue Bonds, Series 2024A

- $27,225,000 Public Facility Refunding Revenue Bonds, Series 2024B

- $128,070,000 Public Facility Revenue Bonds, Series 2024C (Federally Taxable)

In 2024, this author wrote an 11-part series on the multiple scandals surrounding the Virginia Beach City Council’s actions to fund Atlantic Park. Atlantic Park is comprised of:

- the Dome entertainment venue and the parking garages owned by the city, from which it hopes to generate revenue,

- all the steady revenue-generating assets like restaurants, shops, and apartments owned by a private development company,

- a maybe-not-revenue-generating wave pool owned by a North Carolina nonprofit funded with state revenue bonds because neither the city nor the developers wanted any part of it.

In this case, as a Virginia Beach taxpayer, he did not wish to be right in his published prediction that the Development Authority would be unable to service the debt with project revenues.

It turns out he was prescient.