What Goes Up Stays Up

Share this article

ADVERTISEMENT

(comments below)

Comments

Comments

22 responses to “What Goes Up Stays Up”

-

Small builders are not likely to sell a 2×4 they paid $10 for last spring for $5 today. It is reasonable to expect they will seek to recover the full cost of the materials already on hand. Prices will come down as expensive inventory is depleted and competition takes hold. The same is often seen on service station pumps, where there is a delay in price declines after a big run up in prices. Station owners have to pay for the expensive fuel in their tanks before they can make significant reductions. Competitive pressure always brings prices into line.

-

The price of something is almost never dictated over the short term by the cost of the components. The price is set by supply and demand. Here in NoVa the housing market is on fire. Why? Supply and demand. The supply is low due to slowdowns in building during the pandemic. The demand is high as people (particularly first time homebuyers) who put off buying a home during the economic uncertainty of the pandemic now are aggressively in the market given that the pandemic is presumed to be over (or close enough to over).

Beyond that, the new houses going on the market now were built from lumber contracted for last spring when the costs were high.

-

To Ronnie and DJ: I just discovered that, instead of linking to a WSJ article and a RTD article, I linked twice to the RTD article. Here is the WSJ article:https://www.wsj.com/articles/lumber-prices-are-way-downbut-dont-expect-new-houses-to-cost-less-11626260401?mod=hp_lead_pos4

Also, here is a quote from that article:

An analyst recently asked KB Home Chief Executive Jeffrey Mezger on a conference call if the big home builder would share lumber savings with house hunters—lowering an average asking price that rose 13% to $409,800 during its fiscal second quarter ended May 31—or boost margins, which have climbed to their highest levels since 2006. “It will depend on the competitive landscape in each city,” Mr. Mezger said. “But our hope and expectation is we’ll take it to margin.”

The WSJ cited another specific large home builder as saying that margins would be larger.

I tend to agree with your arguments, but, who am I to argue with the WSJ?

-

To Ronnie and DJ: I just discovered that, instead of linking to a WSJ article and a RTD article, I linked twice to the RTD article. Here is the WSJ article:https://www.wsj.com/articles/lumber-prices-are-way-downbut-dont-expect-new-houses-to-cost-less-11626260401?mod=hp_lead_pos4

Also, here is a quote from that article:

An analyst recently asked KB Home Chief Executive Jeffrey Mezger on a conference call if the big home builder would share lumber savings with house hunters—lowering an average asking price that rose 13% to $409,800 during its fiscal second quarter ended May 31—or boost margins, which have climbed to their highest levels since 2006. “It will depend on the competitive landscape in each city,” Mr. Mezger said. “But our hope and expectation is we’ll take it to margin.”

The WSJ cited another specific large home builder as saying that margins would be larger.

I tend to agree with your arguments, but, who am I to argue with the WSJ?

-

The Wall Street Journal confirms my argument – it is about supply and demand, not component costs.

When Mezger says, “It will depend on the competitive landscape in each city.” he is essentially saying that if demand exceeds supply he will not lower prices. He then confirms this by saying that he hopes to take the benefit to margin.

This is a timing issue. Once the homebuilders get back to full capacity and supply equilibrates with demand it will not be possible to charge a 13% premium over your competitors. Until then, they will charge whatever the market will bear.

I feel sorry for those first time homebuyers who are so anxious to finally buy that home (post-COVID) that they are willing to rush out and pay a premium. If they would just wait a year they will find much better bargains (IMO).

-

There was a study about 20 years ago that looked at the cost of government extractions (impact fees) on housing in California. The study determined that market conditions dictated when and by what amount builder were able to recover the costs of impact fees in the price of new homes. Interestingly, the study also found that it was easire to recover all or more than all of the costs in high-priced homes. Builders often swallowed at least part of the impact fees with lower-priced homes.

-

-

-

You are missing one other cause. Companies like Redfin, Zillow, and others are snatching up low cost homes in a “buy and hold” profit scheme. They’re churning the market.

https://slate.com/business/2021/06/blackrock-invitation-houses-investment-firms-real-estate.html

-

They weren’t interested during the period of time a couple of months ago when the cheapest listing in 22408 was my rental townhouse in Fredericksburg…(sold it because I’m sick of being a landlord, there are better ways to use that money).

-

This is what bothers me about politicians like Ralph Northam. He eliminated the Secretary of Technology as a cabinet level position (however, he virtue signaled his wokeness by adding a diversity and inclusion cabinet member). Who in our state government has both the experience and wherewithal along with the stature to analyze the impact of what Zillow and Redfin have on the market? It’s partly financial – they can borrow cheaply. However, it’s also a matter of data and algorithms (i.e. machine learning / AI). How might the combination of these two things impact the Virginia housing market? Well, that requires not only the ability to understand the present set of capabilities but the ability to predict the pace of improvement in those capabilities. Who you gonna call?Tommy Norment?

Meanwhile, Zillow’s stock price has increased 10X over the past 10 years.

Rather than get a handle on this now our technologically blind state government will do nothing until it’s “crisis time” and then will cobble together some half-assed band-aid designed to solve the problem.

-

This is more crude. It’s market manipulation. This isn’t an AG-first job. It’s USA’s job. These companies are buying and selling houses like stock shares in short term transactions to drive the market price.

-

-

Not much different than cornering any other commodity market is it?

-

Nelson, William and Lemar Hunt ride again?

I find it hard to consider housing a commodity like silver. Much more relevant data about homes than about silver. However, attempting to corner (or even notably impact) housing has huge public policy implications in my mind.

As for Redfin and Zillow executives, take heed ….

In February 1985 the Hunt brothers were charged “with manipulating and attempting to manipulate the prices of silver futures contracts and silver bullion during 1979 and 1980” by the United States Commodity Futures Trading Commission (CFTC)

In September 1988 the Hunt brothers filed for bankruptcy under Chapter 11 of the Federal Bankruptcy Code largely due to lawsuits incurred as a result of their silver speculation.

What is Virginia’s equivalent of the CFTC for housing manipulation?

-

Nope. Actually it’s more a “pump & dump”.

-

-

They weren’t interested during the period of time a couple of months ago when the cheapest listing in 22408 was my rental townhouse in Fredericksburg…(sold it because I’m sick of being a landlord, there are better ways to use that money).

-

…and better ways to be perpetually irritated.

😉

-

I had a management company which dealt with most of the irritation. Of course, there was a bit of irritation upon finding out that the tenants ripped several interior doors off their hinges and punched holes in the walls and the security deposit won’t cover the repairs, among other things.

It was enough to make me think that there’s a segment of the population that needs to be living in rental quarters built with vandal-resistant finishes much like a prison.

-

If we ever get together for a few beers someday, ask me to tell you the whole story of a rental house my parents owned for a brief period. You will be horrified.

The memories of the things we found in that house after my dad evicted one particularly bad tenant will be with me forever. One “teaser” example: The tenants had a dog. Even though the house had a fenced back yard, the dog never went outside – ever. They kept that poor animal locked up in one of the bedrooms 24/7 – and they never once cleaned up the messes it made in that room during the +/-12 months they lived there. The foulness was at least three inches deep over the entire surface of the parquet hardwood floor.

After we literally shoveled-out the room, we left fans blowing across the floor for a week to dry it out, and then Dad spent 8-10 hours with a floor sander trying to get rid of the stains. I think he sanded away about half the thickness of the wood before it was suitable to be refinished. And that was not the worst of what these people left behind.

I was about 10 years old at the time, and to this day I still find it difficult to believe that human beings can/will live the way those people lived in that house.

-

-

-

Redfin & Zillow are just brokerage companies, they don’t own or buy and sell houses. I don’t know how NN derived that information from what he linked as neither is mentioned out side of sale data in his citations.

-

-

-

what effect does the mortgage deduction have on this issue?

-

For homeowners or landlords?

-

-

St. Louis Fed President James Bullard made similar comments on Monday when he told the Wall Street Journal that he was worried that the central bank purchases risked overheating the housing sector.

“I am a little bit concerned that we’re feeding into an incipient housing bubble…I think we don’t need to be doing that with the economy growing at 7 per cent,” Bullard told the Journal.

Yellen’s meeting with Powell will be the first time that the Financial Stability Oversight Council (FSOC) discusses concerns about the housing market in a substantial way, the Bloomberg report added, citing sources.

-

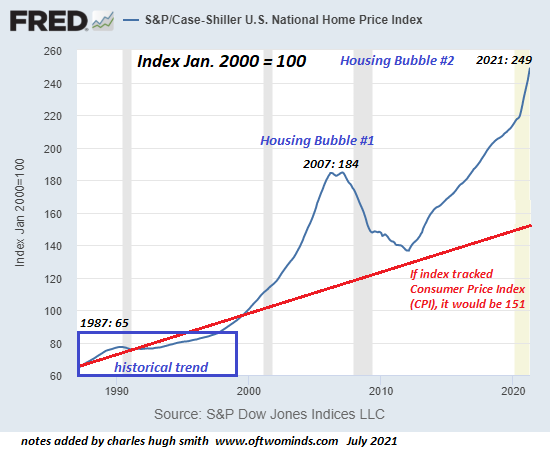

And up, and up, and up…

https://d1-invdn-com.investing.com/content/pic8968b0b8ac49ee4935e52a68eeda6523.pngInteresting graphs against an extrapolated “CPI” for housing prices and includes rents. Of course, the CPI projection they create ignores the fact that CPI includes housing, so it’s just comparing housing costs againt a linear extrapolation of the past housing costs. Meh.

https://www.investing.com/analysis/housing-bubble-ready-to-pop-200590558

{kind=link}

Leave a Reply

You must be logged in to post a comment.