by Dick Hall-Sizemore

When I moved to Richmond in the early 1970s, fresh out of graduate school, my wife and I rented a house for a couple of years. Then, with the help from my in-laws with the down payment, we purchased a “starter” home—a three-bedroom, one-bath, brick rancher, much like the one we had been renting. We did this on only one income, mine, as we had a small child and my wife wanted to be a stay-at-home mother.

Such a scenario is probably inconceivable today. There has been much concern and discussion, nationally and on this blog, about the cost of housing and the need for “affordable” housing. The Wall Street Journal had a recent article that neatly summarized many of the underlying causes for the lack of affordable starter housing. For those BR readers who do not have access to the Journal, following is a summary of the main points made, along with the charts provided.

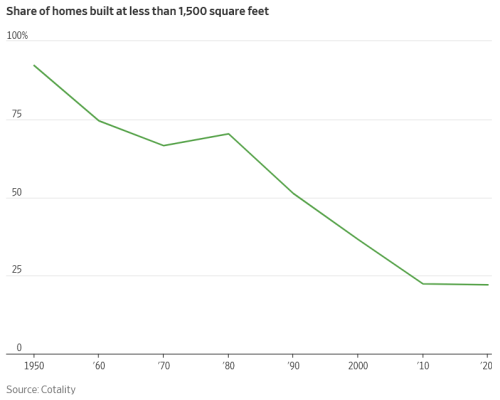

First of all, over the last 70 years, the proportion of new housing stock that would qualify as starter homes has steadily decreased. As shown in the chart below, 92 percent of the new homes built in 1950 were under 1,500 sq. ft. By 2020, that share had dropped to 22 percent.

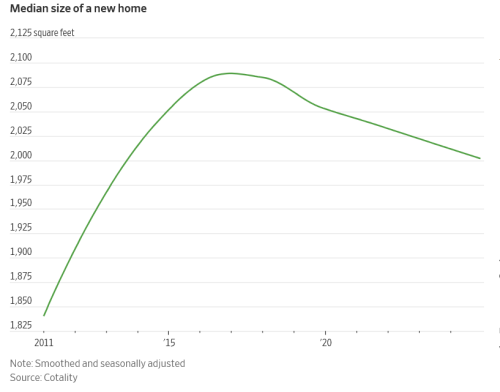

Not only were there fewer new homes with under 1,500 sq. ft., builders were putting up bigger and bigger houses, as shown in the chart below. In 2010, the median size of a new home was 1,850 sq. ft. By 2017, the median size had grown to 2,100 sq.ft. Since that 2017 peak, the median size has decreased to about 2,000 sq.ft. in 2024, still significantly larger than the median house 14 years earlier.

The reason for the increase in house size is straight forward. As the Journal puts it, “It is harder for builders to make money on smaller homes.” Much of the underlying costs, such as land and utility connections, are the same regardless of the size of the house. The cost of building supplies has risen significantly in recent years. As a result, with a smaller house, buyers will not experience a proportionate decrease in cost.

An example from my neighborhood illustrates this dynamic well. The neighborhood consists of a lot of starter homes, built in the 1950s, three-bedroom ranchers and Cape Cods (mine included), along with larger two-story houses. One of the last vacant lots in the neighborhood recently came on the market. Reportedly, the buyer (a contractor) paid about $175,000 for the lot. Needless to say, the contractor was not going to build a small rancher or Cape Cod on that lot. A two-story house with an estimated 2,000 sq. ft. is going up there now.

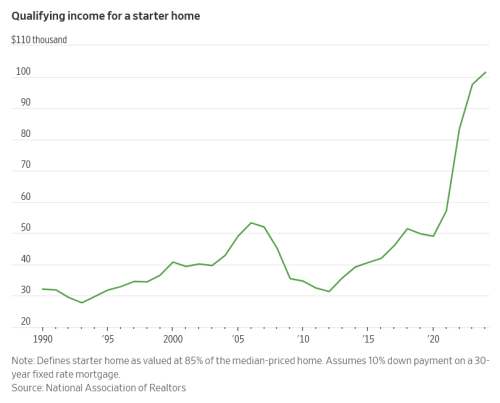

As if the increased size of houses and the rising cost of building materials were not enough to put “starter” homes out of the reach of first home buyers, there was a buying rush during the pandemic with the shortage of available houses driving up prices. The table below shows the result. In 1990, a buyer with an annual income of $32,000 could qualify for a loan for a starter home. The qualifying income increased to $53,000 in 2006, but, during the Great Recession that started in 2008, an income of $31,000 in 2012 would enable a prospective buyer to qualify. The level of qualifying income steadily increased to $49,000 in 2020. After that, it shot up sharply. In 2024, due to increased prices and higher mortgage rates, a prospective buyer of a starter home needed an income of over $100,000 to qualify for a loan. According to the Journal, the median price of a starter home “rose to $287,000 in 2024, up by about 44% from 2020.” Over these years, wages have risen, of course, but not at the rate of the increase in housing costs.

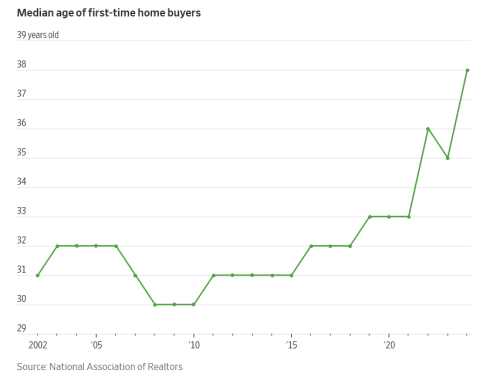

The combination of all these factors—few smaller homes being built, increased median size of homes, increased building costs, and higher mortgage rates—has resulted in people having to put off buying that first house. The last chart illustrates this dramatically. In 2002, the median age of first-time home buyers was 31. That dipped slightly during the Great Recession, then gradually increased to 33 in 2020. After that, there was a dramatic increase, with the result that the median age of first-time home buyers in 2024 was 38.

What is the answer to this dilemma? The Journal does not offer any answers in this article, and I don’t have any. I am just glad that I came along when I did.

Leave a Reply

You must be logged in to post a comment.