by James C. Sherlock

Sometimes, when you are winning big in a table stakes poker game, it can be time to put some money in your pocket. That is part of the game many nursing home chains are playing these days.

Everybody wins but the nursing facility residents, Medicare, and Medicaid.

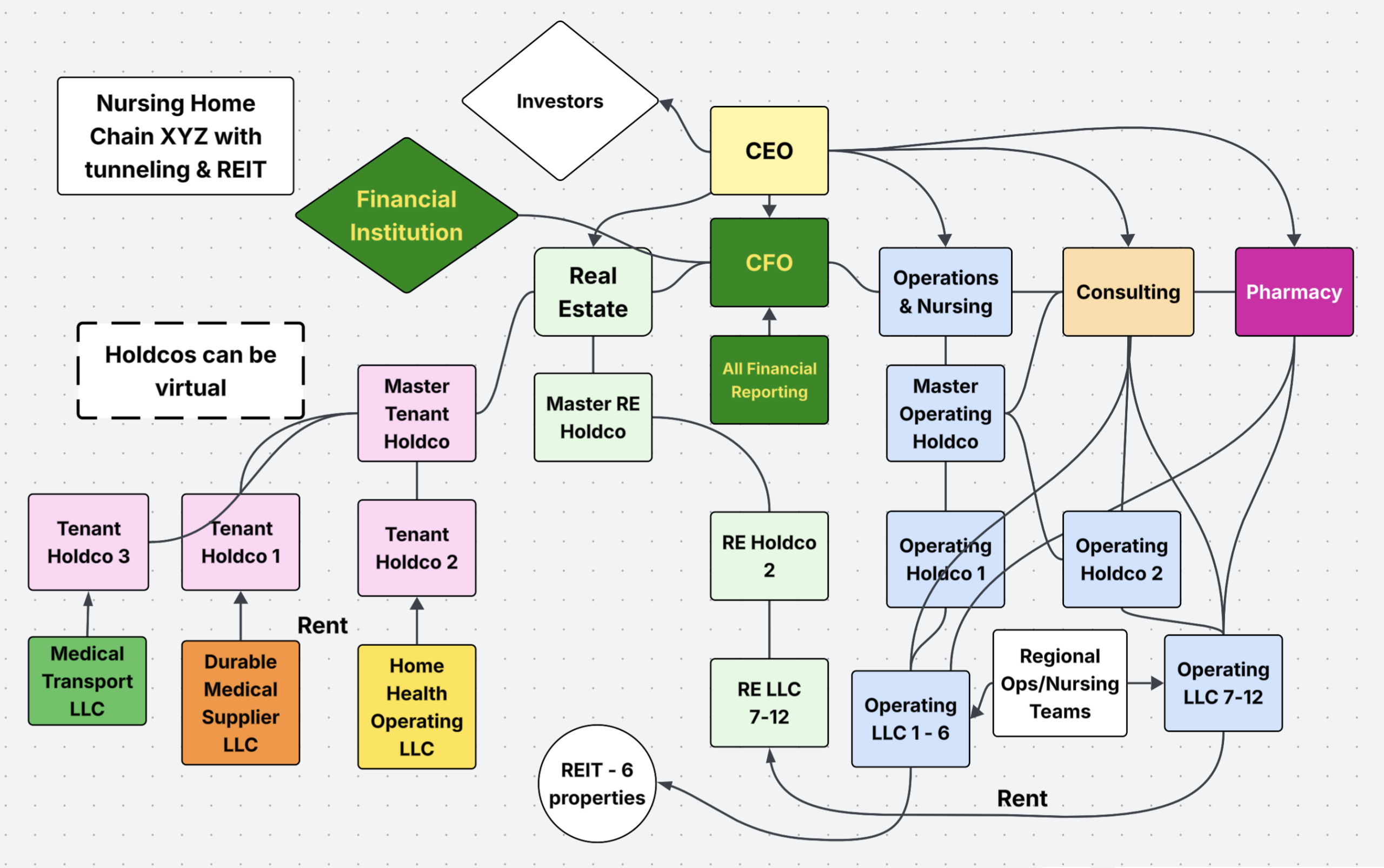

The enterprise architecture of many less ethical chains is familiar to regular readers. In this example, a chain has sold six of its property LLCs to a real estate investment trust (REIT) and kept six.

The business model is as profitable as it is complicated, and for the same reasons. Notice all the places where Medicare and Medicaid money go each day in this example. Not much is left for staff and patient care.

Compared with other states, Virginia’s nursing home sector has been sparsely penetrated by REITs. We can view this as the owners of the chain-controlled operating companies and property companies that dominate in Virginia being very happy with their profits, the COPN-driven lack of competition, and Virginia’s history of non-enforcement of regulatory violations. We give them few reasons to sell their property companies.

But some do. We’ll look at the players, the deals, and the implications.

The players

The nation’s largest healthcare REIT, Welltower, owns only high-end retirement community properties in Virginia, all of which are leased to operators such as McLean-based Sunrise Senior Living.

The REIT that is the biggest player in Virginia nursing homes is Omega Healthcare Investors, Inc. (NYSE: OHI). That $13.3B market-cap company owns 24 properties with nursing facility tenants in the Commonwealth. The sellers and OHI tenants tend towards national-scale chains like Saber and Ciena.

A relatively new player in the Commonwealth is CareTrust REIT, Inc. (NYSE: CTRE), with a market cap of $8.3B. It owns, acquires, develops, and leases skilled nursing, senior housing, and other healthcare-related properties.

Medical Facilities of America (MFA), dba Lifeworks Rehab, is Virginia’s largest chain. MFA and YAD Healthcare each operate in Virginia and North Carolina. Their headquarters are located across the street from each other in Lakewood, New Jersey. They have begun testing the REIT waters together.

CareTrust closed several deals in the past two years to buy property companies from those two chains.

- May 15, 2024, included eight MFA and four YAD properties in North Carolina.

- MFA’s Glenburnie Health & Rehabilitation in Richmond on August 29, 2024.

- December 12, 2024, another MFA property in North Carolina.

- October 30, 2025, MFA’s Culpeper and Pulaski Health & Rehabilitation Centers in Virginia and one MFA facility in North Carolina.

- MFA’s Bayside Health & Rehabilitation in Virginia Beach (date unknown).

MFA and YAD continue to operate those 17 nursing facilities as CareTrust tenants. Of the 13 MFA properties sold to the REIT, 12 have Medicare Compare one-star staffing. The other, in North Carolina, is a Special Focus Facility (SFF). Of the four YAD facilities, three have 2-star staffing ratings, and the other is an SFF. So, there is perhaps higher-than-normal tenant risk there for CTRE.

The deals

The properties are covered by Master Lease Agreements. The agreements feature triple-net leases under which the tenant pays a lower base rent but also pays all three primary property expenses: taxes, insurance, and maintenance (including repairs and capital asset maintenance).

In making the deal:

- CareTrust’s considerations would have included the fact that REITs have experienced large-scale defaults among some large-chain tenants in the past. CareTrust has a very large portfolio, nearly all of which consists of nursing homes with tenants rated higher by Medicare Compare than these, so it likely would have sought rent payments high enough to offset the risk.

- The two chains are taking money off the table. The capital gains can be reinvested or distributed to owners. Given their low-staffing, high-occupancy business models, the sellers should have had ample cash flow from the properties to negotiate and pay rent. Higher rent equals a higher sales price. It is unclear how far the two chains will extend their property sales.

The implications

These deals should be of interest to regulators, but it is not clear how they could pay attention. State regulators, the Virginia Department of Health and the Department of Medical Assistance Services (Virginia Medicaid), don’t have the information. Their focus has in the past been exclusively on the individual operating companies.

That will work until it doesn’t.

Virginia and North Carolina regulators have already allowed each state’s nursing facility portfolio to be measurably degraded by out-of-state chains. REITs, like chains, regularly churn their portfolios. Instability harms residents. When ownership changes, staff changes are likely, suppliers change, and residents’ living and care conditions are often thrown into turmoil.

Bottom Line

Two recommendations:

- Unfortunately, our elected officials and their executive branch appointees may be as surprised by a major default by a chain or REIT operating here as they were by the Colonial Heights scandal. They need to gather information on the chains and REITs, assess the scope of potential issues, and plan for a default.

- Since all the players are dividing up Medicare and Medicaid money, it’s time for the state to pay attention to where it’s all going and act on cases of fraud before the feds come here and do it for us.

Leave a Reply

You must be logged in to post a comment.