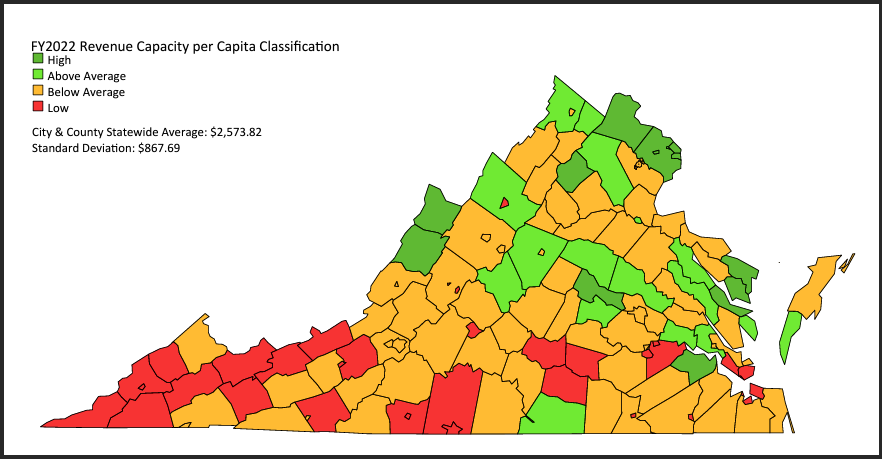

A concept related to “fiscal stress” (see previous post) is “revenue capacity.” The Commonwealth of Virginia defines “revenue capacity” as the amount of revenue a local government would generate if it set its tax rates at statewide averages. The calculation takes into account five main revenue sources: true value of real estate, true value of public service corporation real estate, registered vehicles, local option sales tax receipts, and adjusted gross income. The state Commission on Local Government expresses the resulting number on a per capita basis.

The index compiled by the Commission, based on the most recently available numbers from FY 2022, ranges from a high of $5,886.10 in Bath County and a low of $1,272.16 in Radford City. The average revenue capacity per capita in the Commonwealth is $2,960.72.

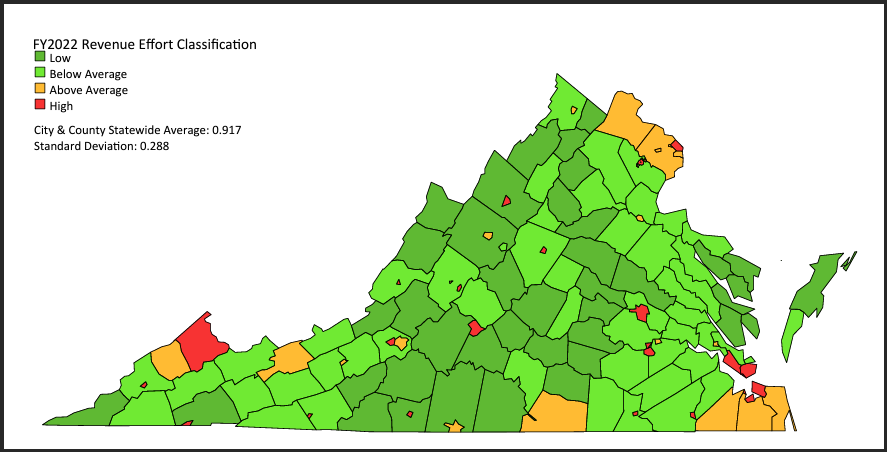

The Commission then calculates what it calls “revenue effort” — how much revenue a locality raises expressed as a ratio of its revenue capacity, as seen in the map below:

From this map, we can see which localities are willing to tax themselves above and below their means.

Whether expending greater revenue “effort” is a good thing or bad thing will depend largely upon (a) your ideological views toward taxes; and (b) the perceived value of government services delivered.

As a rule, cities have higher taxes than surrounding counties. Historically, the discrepancy arises from Virginia’s local-government structure devised in the 19th century when cities were urban, counties were rural, and the concept of suburbs did not exist. The state constitution empowered cities to raise more taxes in order to provide the higher level of services demanded by urban residents. Since World War II, the rise of the pattern of scattered, lower-density development that we call the suburbs fudged the distinction between urban and rural, and incremental changes to tax laws and public financing have largely erased the differences in revenue sources and taxing powers.

It would be helpful if the Commission on Local Government displayed one more data set: actual taxes collected per capita. The disparity in tax burden between cities and outlying counties is one of the factors, along with schools, crime, walkability and other amenities, that influence where people choose to live and locate their businesses.

— JAB

Leave a Reply

You must be logged in to post a comment.