By James C. Sherlock

The surf park jumps right out at you. It is meant to.

It will be the first surf pool in the mid-Atlantic region. The other components of Virginia Beach’s Atlantic Park will depend upon it to create buzz and draw visitors.

A developer group led by Venture Realty Group initially planned to own it. In September of 2020, prior to formal design plans, the team met a deadline to prove it could secure the necessary financing.

Costs rose with inflation in 2021 and 2022. Delivery dates were rescheduled with WaveGarden, the Spanish manufacturer of the wave-pool machinery, pushing production of the Virginia Beach equipment behind orders from other customers. Councilman Moss warned the council in public session that the project needed to be reconsidered in the face of inflation in commercial construction costs.

By 2022, those inflated construction costs were known. Revenues and operations and maintenance costs were estimates. The Virginia Beach surf park is small by industry standards, and thus capacity constrained. Very high utilization rates will be required to pay the bills.

The developer team missed a financing deadline because of the surf park. they gave the rights to a North Carolina 501(c)(3) to access tax exempt municipal bonds. They formed Venture Waves Surf LLC on September 13, 2022 to deal with the problem before government bond authorities.

By the time the issue was officially referred to Virginia Beach, Venture Realty’s Mike Culpepper, lead developer spokesperson, already had testified before the Virginia Small Business Financing Authority in a successful attempt to get that public charity state municipal revenue bond financing.

Mr. Culpepper later told the press that access to tax exempt bonds had been the strategy “for more than two years”.

After the bond issue was unanimously approved by the state Authority’s board, the Virginia Beach Development Authority passed a resolution that gave city authorization to a state decision that had already been made. It helped satisfy SEC and IRS requirements for the bonds. Mr. Culpepper was there to answer questions.

A North Carolina public charity. In 2022, the developer team engaged North Carolina-based 501(c)(3), P3 Foundation to fund and own the surf park. P3 in the title stands for Public-Private Partnership, the specialty of that organization.

The charitable mission of P3 Foundation reported to the IRS is “to partner with public and charitable entities to develop services, activities, and programs designed for senior housing, education, health care facilities, affordable housing, and governments.“

That same Form 990 reported a negative net worth. Net assets had grown increasingly negative each year. Three existing projects showed a cumulative loss. It had never financed recreational facilities.

Charity Navigator currently rates P3 Foundation “very poor” — zero stars. From that assessment comes the following chart:

So, P3 Foundation was an unlikely candidate to which to lend new money to build a surf park.

But they found mortgage lenders for that facility at the Virginia Small Business Financing Authority (VSBFA) which had three enticing characteristics. It had no standards for the ability of a borrower to repay the obligations, no limits on the bonds that supported 501(c)(3)s, and it was under General Assembly pressure to move money out the door.

The dates of the actions happened in an unusual order

- On September 13, 2022, the VSBFA board approved a very high yield bond issue for the surf park.

- The Virginia Beach Development Authority resolution authorizing the state authority to issue the bonds was approved on September 20, 2022.

- On October 5, 2022, P3 Foundation registered P3 VB Holdings, LLC with the Virginia State Corporation Commission. A disregarded entity under IRS rules, it was effectively a division of the parent company. On that date the new company with no employees possessed only the rights to build the surf park. And it was officially a Virginia 501(c)(3) small business qualified for the tax exempt Virginia municipal bonds.

In March of 2023, VSBFA issued unrated municipal bonds for that new company with a face value of $63.575 million.

Bloomberg’s Eliza Ronalds-Hannon has recently published an article about covenants in high yield debt.

A covenant in debt financing is an agreement that gives creditors tools both to nudge a borrower away from overly risky activities and to recover as much of their money as possible should the company go bust. On the preventive side, it places limits on things like a company’s ability to take on additional debt or pay dividends to shareholders, or requires a company to provide regular financial information to investors or keep its earnings high enough to cover interest payments.

Such pledges can seem incidental to eager lenders when the economy is strong. But when financial troubles arise and companies seek more cash to weather what they hope is a temporary crunch, covenants that limit new borrowing or restrict what assets can be mortgaged become a serious impediment — as intended.

The covenants found in the surf park bond memorandum are both proscriptive and prescriptive in exhaustive detail.

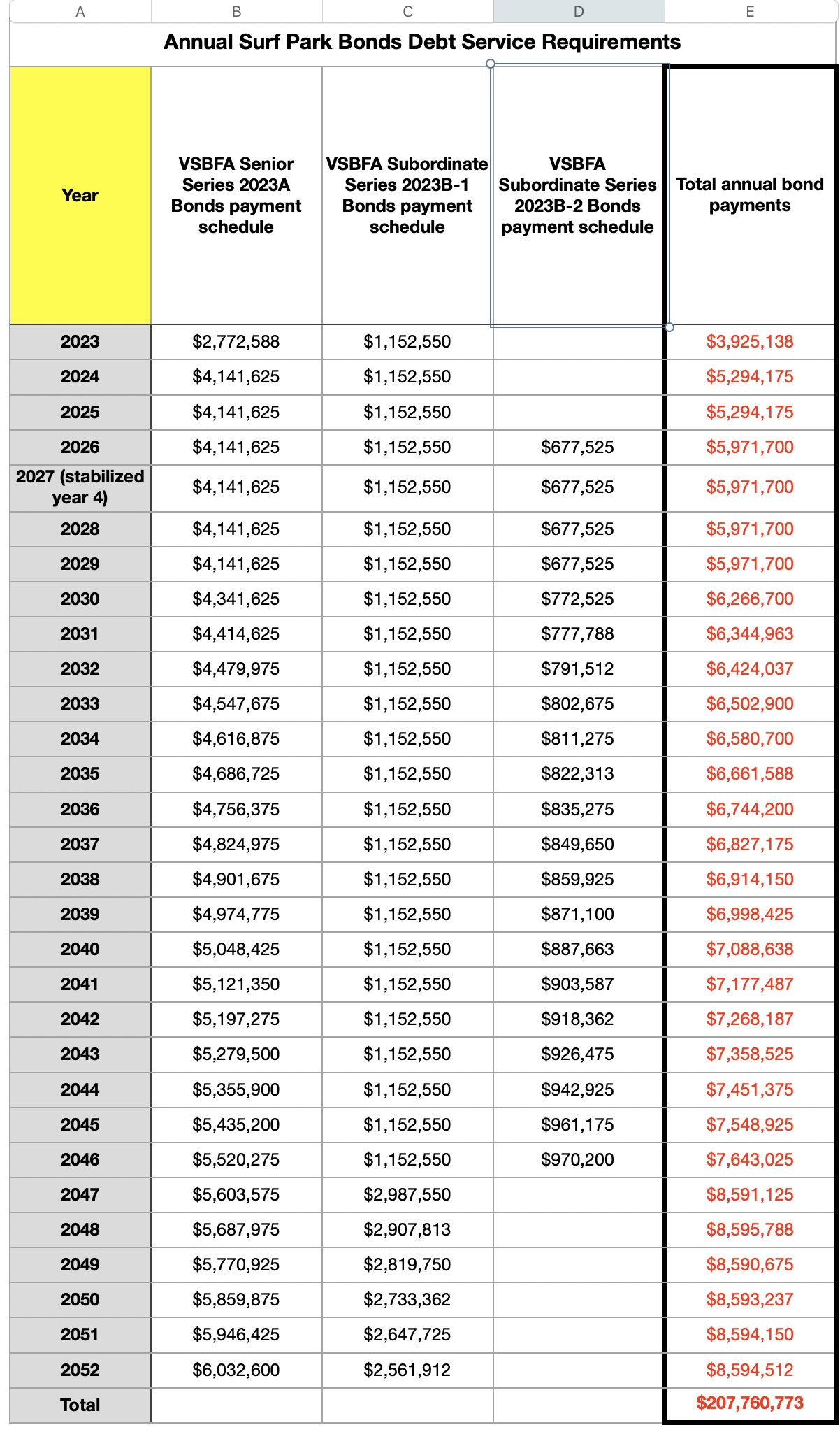

The tax-exempt senior issue was sold to professional investors at a discount to yield 9%. The subordinate issues were sold to members of the developer team with yields of 9.25% tax exempt and 10.25% taxable. Those appear to represent the highest yields on any Virginia municipal bonds currently in circulation.

The debt payment schedule is below.

The 2023 bond documents (download here) offered twelve pages of surf park investment risks that were summarized in Part 5 of this series.

VSBFA offered that it “has not endorsed and is making no representations of any kind regarding the creditworthiness of the borrower or the ability of the borrower to repay the … bonds.” It did not reveal that its rules do not require it to care.

With that transaction, the developer, who would now be paid to manage and operate the surf park, turned a liability into an asset.

But it added a great deal of risk to the overall project.

Financial Risks.

As described in the bond documents:

- Consultant Colliers had provided a 10-year cashflow forecast. It predicted annual use by 80,000 surfers and 120,000 others paying to watch. That represents an average of 77% of total surfer capacity in the lagoon 12 months a year. Surfers, mostly local, were expected to pay up to $159 an hour to generate the revenue predicted in the study.

- The developer offered a more positive cashflow forecast without details of its differences in assumptions. The actual pricing of surf park admissions is as yet undefined.

- By the declarations in the documents, no one is held responsible if neither estimate proves accurate.

A risk from the surf park to the financial feasibility of the entire Atlantic Park project was described as follows:

Many of the life-style tenants and restaurants that have expressed interest in the project may be dependent on the surf park or a similar anchor tenant/amenity to drive adequate traffic to produce the retail sales necessary to justify the proposed rents.

Professional investors employed by Virginia muni bond funds bought the senior series. Default was a distinct possibility. The bond yields signaled that the buyers — and the state bond authority — knew it.

Commentary. The surf park is the asset of Atlantic Park upon which most of the rest of the project depends for profitability.

It is now owned by P3 VB Holdings. With no money of its own, the new entity had to borrow not only the construction money, but amounts required for reserves, working capital, capitalized interest, costs of issuance and other financing expenses related to the issuance of the Bonds.

It now has three mortgages whose combined principal represents 150% of the cost of construction.

No one has actual figures, only projections, for how many people will pay a forecast $89 to $159 per hour year round to use the facility or how many others will pay $20 to watch other people surf. Actual pricing has yet to be announced.

The options to increase net revenues appear limited.

The wave pool is small by industry standards, so capacity is constrained. The water will not be heated for the cold months because the cost of heating a three acre pool would be staggering. The surfers are forecast to be mostly locals.

We’ll all have to see.

By the language of the bond offering, P3 Foundation is shielded from obligations on the P3 VB debt. But the tax exemption of the bonds remains dependent upon P3 Foundation maintaining its tax-exempt status. Should it lose that status, the surf park will be forfeited and the bond trustee will sell the assets.

The VSBFA board had the authority to approve the unusual financial structure, but it may prove difficult to explain why this deal for this borrower with this repayment risk was considered an appropriate use of Virginia municipal bonds.

On the very same day the state bonds were sold, the city sold revenue bonds for pre-construction infrastructure.

A good question, if VSBFA board members asked it, is why the City of Virginia Beach did not write the bonds or directly fund and own Atlantic Park’s signature venue and instead backed the P3 Foundation deal and asked the state to fund it.

Leave a Reply

You must be logged in to post a comment.