Commentary by James C. Sherlock

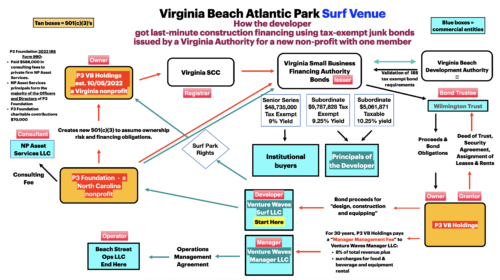

A last-minute search for surf park financing delayed project construction for a year. Neither bankers nor the City of Virginia Beach wanted any part of it. The developer missed a funding deadline. The city forgave it, but the pressure was on.

So, with city backing:

- The developers, organized in this case as Venture Waves Surf LLC, contacted 501(c)(3) P3 Foundation in North Carolina, which is in the business of participating in public private partnerships. It accepted the rights to the venue.

- P3 and Venture Waves Surf contacted the Virginia Small Business Financing Authority, which is by policy a soft touch for non-profits. It agreed to issue tax exempt junk bonds. The yields were necessarily so high to attract buyers that the P&I debt load for that small surf park is $207 million. There is subsequently a significant risk recognized by the bond press (Bloomberg) that surf park operations and maintenance costs and debt payments together may prove more money than it will generate. They called it a speculative bet. If that happens, the surf park will be in default and put the whole project in financial jeopardy.

- P3 Foundation established a Virginia 501(c)(3) subsidiary, P3 VB Holdings, to qualify as the borrower. It has no employees.

- The subsidiary paid the developer to build the venue and will pay them to manage and operate it.

The journey was so complex and wandering that it needs a graphic to explain it, so the author created one.

Those players and their interactions will be discussed in following parts. Their participation both revealed and generated issues and actions that were not in the public interest.

It never needed to happen.

P3 Foundation and the Virginia Small Business Finance Authority (VSFBA) need never have been involved with Atlantic Park.

By July of 2022, the city had all the leverage it needed to modify the contract to its advantage. Read what the public knew from a TV 10 report:

(Atlantic Park) continues to move forward, even though a binding agreement can now legally be ended.” … “Taxpayers would fund roughly $110 million of the deal”. … “The June 1 deadline was missed, which per the development agreement, gives the Virginia Beach Development Authority — the owner of the land — the right to terminate the deal if they wish. .. (emphasis added)

If the deal had been terminated by the city for cause:

- developers would have owed a lot of money to their bankers; and

- the city would still have its land, all of the taxpayers’ money committed to Atlantic Park and whatever developer money was owed in the default terms of the agreement.

The city could have offered a new deal in lieu of termination of the one it had. The developer would have had no choice but to accept it.

But, from the same article,

However doing that (termination) has never been suggested.

“The June 1 date was simply a waypoint that was established in our negotiation,” Tiffany Russell, a spokesperson for the City of Virginia Beach, said. … Mayor Bobby Dyer has said he doesn’t believe the public-private partnership is at risk of failing as the proposed Oceanfront arena did several years prior.

An alternative path. In 2022, the city’s Tourism Investment Program (TIP) Fund had a cumulative fund balance/capital reserve of over $42 million. The surf park is costing $41 million to build.

City Council could have offered to relieve the developer of the surf facilities. The surf park would have operated mortgage free.

Cash flows without the bond repayment overhang would have been available to the city to help pay the service on the other bonds issued for the project, to repay the TIP fund, or for General Fund purposes.

The developers would still have been left with the very low price they negotiated for 309 apartments, in excess of 100,000 square feet of retail, restaurant and office space and all of the food and drink concessions. Importantly, they would have been sure that the surf park, so necessary to the value of those investments, would remain open.

Under such a new contract:

- the public-private development deal would have been considerably more balanced than today. Taxpayers would own the surf park and its mortgage-free cash flows;

- VSBFA and P3 Foundation would never have been involved; and

- The surf park, owned by the city, would stay open.

Didn’t happen.

Instead the 501(c)(3) borrower started with nothing. It needed bond proceeds not only to fund construction, but also for reserves, working capital, capitalized interest, costs of issuance and other financing expenses related to the issuance of the bonds.

Now the overhang of the surf park bond service may put the entire project at risk. The borrower owes over $207 million in principal and interest after he pays all of the costs to keep the surf park operating and maintained.

Taxpayers are left to wish him good luck.

Bottom line. The surf park bonds have become perhaps Atlantic Park’s biggest risk.

Part 8 will show why.

Leave a Reply

You must be logged in to post a comment.