Updated September 18 at 10 AM and 3:16 PM

By James C. Sherlock

Atlantic Park is under construction as a massive new entertainment district near the oceanfront in Virginia Beach’s resort area. The centerpiece, a surf park, will be surrounded a 3,500-seat concert hall, shops, restaurants, offices, and apartments.

If it succeeds, Atlantic Park will transform the resort district of Virginia Beach and generate additional tax revenues for the city.

But the City Council early on rejected a plea from the city manager to be able to “tell them it will pay for itself” and never looked back. Council never asked for a city business plan, perhaps because it would have served as a rebuke as spending on the project spiraled out of control.

In 2023 city officials were forced by SEC requirements for a city bond issue to publicly acknowledge the manifest economic risks to Atlantic Park, but did so only buried in a 900+ page bond prospectus. Those risks, which led a report in Bloomberg in review of that bond issue to call Atlantic Park a “speculative bet,” would have ruined the story.

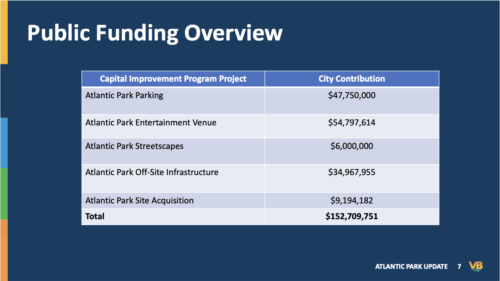

Here are two views of city spending. First, a slide presented to city council on May 28 of this year.

But the city borrowed the money.

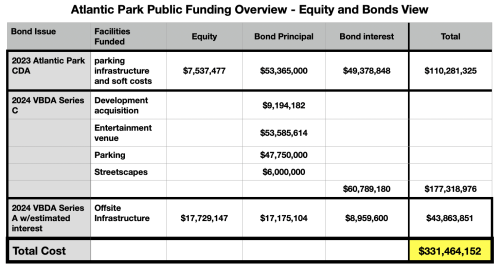

A second slide below is compiled by the author from the documentation of three series of bonds issued in 2023 and 2024 which city bond authorities must repay through providing money from revenues for city appropriations:

That view shows the city at over $300 million in equity and debt for what the council slide called $153 million in city contributions.

Expensively improved city land worth $40 million is leased to the developer at a dollar a year for up to 100 years. Four hundred parking spaces that cost $30,000 each to build are also leased to the developer for a dollar a year plus contributions to a maintenance fund.

This series will tell the story of how we did it, but not why.

As befits the largest public-private partnership in Virginia Beach history, the Atlantic Park lead developer, Venture Realty Group, has assembled a powerhouse team. It includes some of the most influential names in Virginia’s real estate, engineering, architecture, legal and financial sectors.

As the project unfolded over the last seven years, those people sat across the negotiating table from city officials and staff. Their job was to get the best deal they could: the biggest contributions of public dollars, access to municipal tax-free bond financing, and a transfer of as much risk as possible.

They did a very good job.

The city was very obliging.

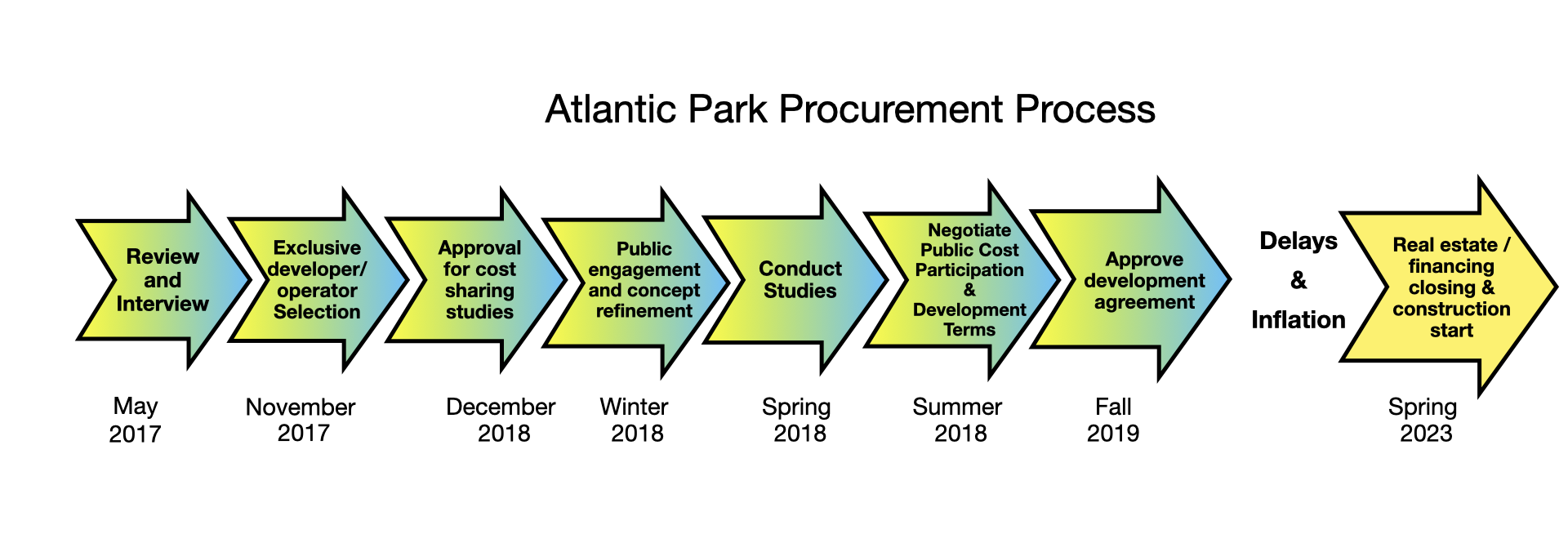

Procurement. A summary of key steps in the Atlantic Park procurement process:

- The exclusive developer/operator was picked in 2017 without a request for proposals ever being issued.

- Two City Council members intervened with the City Manager to increase the developers’ return on costs before the term sheet was signed in 2018.

- City appropriations to the project in the “final” development agreement in the fall of 2019 were to be $95 million to build and operate the concert hall and parking, plus the land the city already owned, plus the parking spaces.

- Construction did not start until 2023.

- The vast majority of city and surf park costs are paid with bond issues. The city P&I going forward is estimated at around $300 million.

- The surf park P&I going forward is $207 million.

- The developers costs are down from the $282 million (2024 dollars) investment promised in 2019 to $116 million plus the interest on their loans and the overhead and opportunity costs spent over seven years of negotiations with the city.

Surf park financing. In 2022, Atlantic Park’s signature surf park proved impossible to finance commercially because of its economic risk.

The developers, with the backing of the city, went for help to a North Carolina 501(c)(3) nonprofit, P3 Foundation, which specializes in public private partnerships.

Together the developers and the nonprofit, again with city backing, went to the Virginia Small Business Financing Authority (VSBFA) for tax-exempt municipal-bond funding.

VSBFA proved undeterred by P3 Foundation’s North Carolina location, negative net worth, and history of unsuccessful investments. It is possible that board members did not know of that record. Notably, current Virginia Private Activity Bond Guidelines contain neither the words “risk” nor “repayment.” By policy, VSBFA factors 501(c)3s with special no-limit borrowing rules.

The board approved the issue unanimously.

After the approval, P3 Foundation established a “Virginia small business” subsidiary to qualify for the bonds. It was a 501(c)(3) shell company with no employees and no assets. But it was eligible for Virginia tax exempt municipal bonds.

Those bonds established senior and subordinate mortgages on the surf park. The total principal and interest is $207 million for a facility that cost $41 million to build.

State financing authority board members knew the economic risks. They authorized the senior bonds to be sold at up to 9% yields and the subordinate bonds at up to 12%. They approved the issue unanimously on September 13, 2022

A week later on September 20th, the Virginia Beach Development Authority (VBDA) passed a resolution that had the effect of satisfying key IRS and SEC regulations for the bonds. See the 2 1/2-minute VBDA board discussion here beginning at the 6:23 mark. It offers perspective on what that board knew and perhaps what it did not know.

Campaign Donations. Virginia permits the making and receiving of unlimited campaign donations. But Virginia Beach has taken it further and decided by local option that very large donations are not declarable conflicts of interest before City Council votes on issues affecting donors.

Real estate and construction interests contributed about $4 million over seven years to sitting council members that constituted 44% of their total donations. Donations gave the real-estate and construction industries outsized influence over how the city spends $350 million annually on infrastructure projects.

Commentary – Virginia Beach City Council, its Development Authority and the procurement process

The issues with the development process trace to the fact that it was completely dysfunctional in design, lasted seven years, had no standards and drifted forward without regard to contracts signed.

The result earns the right to be called the deal of the century — for the developers.

That is the system we have in this city. Virginia Beach citizens need to vote for people who will reform it.

Commentary – distribution of risk

The Atlantic Park project will depend upon the success of the surf park to differentiate their businesses. Major economic risks to the surf park with the mortgage P&I piled on put the entire project in jeopardy.

The developers investments are at the least risk because of the nature of the assets they own and the very low price they paid.

The city paid too much money for owning too little. The city manager in 2018 told city council members that they were spending too much for taxpayers to break even. That was before the city spending spree between 2019 and 2024.

Bottom line.

The author had no concept that his investigation of the public commitments to Atlantic Park would reveal what it did. He only knew that the city’s story did not make sense. There were too many gaps — jump cuts — in the public narrative.

The investigation has revealed that public interests were betrayed at every turn.

Virginia gives local governments great latitude in how they do their business. They can set their own rules for acquisition and for disclosure of conflicts of interest within their governing bodies.

Public private partnerships combined with unlimited campaign donations without oversight of the results lend themselves to inside dealing, opaque financing of development deals, the privatization of profits and the transfer of liability and risks to taxpayers.

Because of where the investigation led, the actions of the Virginia Small Business Financing Authority will be closely examined as well, as will P3 Foundation.

This is a failure of government, not by the developers. The developer team did their jobs in negotiations. They can ask for anything they wish.

In this case, public officials gave away the store.

Update September 11: The performance bonuses agreed to in the 2019 agreement were pledged instead as a source of repayment of city bonds in issued in 2023. ‘

Updates 18 September 2024. Provide specifics of city expenditures of money and property.

Leave a Reply

You must be logged in to post a comment.