by James A. Bacon

Virginia’s healthcare system, like that of the U.S. as a whole, functions as a massive income redistribution scheme from private insurance customers to Medicare and Medicaid patients.

That’s the conclusion I draw from data from a new report, “Tracking Virginia’s 2023 Health Care Spending & Employment Trends,” prepared for the Virginia Hospital & Healthcare Association (VHHA) by OnPoint Health Data.

That’s not what the VHHA chooses to emphasize. In its press release accompanying the report, VHHA touts the finding that private health insurance premiums increased at a dramatically faster rate (22.1% for family policies) than personal health care (PHC) spending (1.2%) between 2019 to 2023.

VHHA also notes that Virginians spent 12.2% less on hospitalization compared to the national average in 2023. If that’s so, it’s a fair point for the VHHA to bring to the public’s attention. We should seek to understand the reason why in the hope that, whatever we’re doing right, maybe we can do more of it. It’s also fair for the hospital trade association to shift blame for rising insurance premiums to the insurance industry. If hospitals have been holding down their charges, they deserve credit for it.

But there’s more to the story. If hospital, prescription and nursing-home spending is stable, why are private insurance rates spiking?

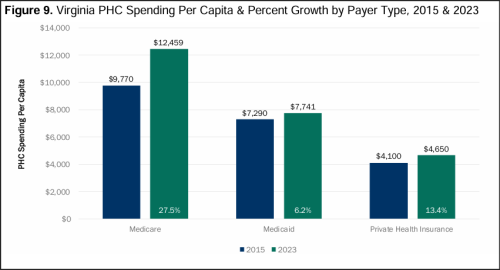

A big piece of the puzzle resides in the graph atop this post. Medicare spending per enrollee amounted to $12,500 in 2015. Medicaid spending per enrollee was $7,700. Private health insurance per enrollee was $4,700.

The disparity should come as no surprise. Medicare patients are older and sicker on average than patients in the other groups. Medicaid patients are poorer and sicker. The employed under-65 set are the healthiest.

While private-insurance customers cost the least, they pay exorbitant insurance premiums. States the VHHA press release: The average individual private-sector health insurance premium in 2023 was $8,133; the average family premium was $24,251.

Let me sum it up for you.

Average cost per enrollee: $4,700

Average premium per enrollee: $8,100

Gap: $3,400 per enrollee

Something is very wrong with this picture.

Don’t blame massive insurance-industry profits. According to the National Association of Insurance Commissioners, health insurers reported profit margins of only 3.3% in 2023. And don’t blame administrative costs. They accounted for only 11.2% of revenues.

What could explain the $3,400 gap between spending and premiums? Here follows my conjecture. We know that Medicare and Medicaid use their monopsony power to force hospitals and other providers to accept lower-than-market reimbursement for their services. Most lose money.

According to the American Hospital Association:

The Medicare Payment Advisory Commission found that hospitals experienced a record-low -12.7% margin on Medicare services in 2022, and it projects that margins will continue to remain near -13% in 20241. Combined underpayments from Medicare and Medicaid to hospitals were nearly $130 billion in 20222, up from $76 billion in 2019.

How do hospitals remain profitable? By sticking it to the private insurance companies, which have less bargaining power than the government monopsonies.

So, reconsider next time you are tempted to think that United Health CEO and shooting victim Brian Thompson had it coming on the grounds that the insurance-industry business model is to make profits by denying treatment to people in need. If that is so, then perhaps the business model of Medicare and Medicaid is to shift their costs to private-sector insurers. Perhaps that’s an angle that OnPoint Health Data would like to explore.

Leave a Reply

You must be logged in to post a comment.