Peeling Back Another Layer of the Grid Modernization Debate

Share this article

ADVERTISEMENT

(comments below)

Comments

Comments

29 responses to “Peeling Back Another Layer of the Grid Modernization Debate”

-

Well all I can say to that, Jim, is ……well, DUH! Yes! They are doing this entirely to reduce shareholder risk and stabilize or enhance shareholder profits. They actually use both debt and equity to finance their capital projects and collect interest on the debt but they only collect a profit margin on the equity. So you are wrong that they will go only for debt.

I suspect under the old regulatory scheme, under the existing non-regulatory scheme, and going forward under this new rip off scheme the company’s credit rating will be excellent as always. But if indeed this scheme ends their need to provide refunds and pushes their actual profit up toward 13-15 percent ROE, thereby reduces their risk and lowers their interest or equity costs – that increases their profit! And given the base rates will never go down they will keep that increased profit! And given any risk of having to share that profit can be eliminated by taking on more debt or equity, the cycle will never end.

http://sg001-harmony.sliq.net/00304/Harmony/en/PowerBrowser/PowerBrowserV2?fk=1179&viewMode=2

Great discussion of the “transformational” regulatory model in todays’ House Commerce and Labor meeting. In particular I recommend the comments of Kim Pate from the SCC staff starting at 4:25 p.m. but Sam Towell from the AG’s office a few minutes earlier was also good.

“While rate payers get their money back on the back end via an offsetting reduction in rate riders, Dominion gets to generate income off that money in the meantime.” Ratepayers get nothing back. Nothing. The utility finances everything either through the rate base or RACS. There will be RACS, probably for every single dime that is not needed to wipe out potential customer refunds.

-

The WAY that Dominion has CHOSEN to go about this is the problem in my view.

It was and is less than up-front ..and the claims about the necessity of Rube Goldberg .. are not believable..

What was broke that needed to be changed so radically? Was the process of trying to upgrade the grid – “broke” under the old SCC regime?

I think it is incumbent on Dominion to “explain” – to the satisfaction of most of the critics.. How many other utility companies are doing this?

-

Bacon,

That you would bring this question to light as you have and invest in being able to explain the rationale is a real public service and part of the great value of this BLOG.

Keep posting as you give this more scrutiny. -

It’s a complex issue and Dominion has their wants and basically wrote the bill.. and the changes as critics have weighed in on it.

Dominion is continuing to give their side of it .. through their surrogates of which – fairly – we would have to say Jim is one.

What I find valuable and needed in Mr. Haners viewpoint – the “con” side.

Having Dominion write the legislation and drive the bus here.. while typical in Virginia is ..in my view … a serious conflict of interest that essentially transfers some of the SCC role to Dominion itself in that because overcharges are directly pipelined for other grid improvements – that Dominion wants vice refunds and a subsequent proposal from Dominion – there is an incentive here for Dominion to overcharge to improve the grid – the way they want to – with less oversight from the SCC.

Perhaps in the modern era of grid energy – regulators like the SCC are an impediment .. an obstacle to efficient upgrading of the grid.. and I actually could buy into some of that – but I need to hear that – a prima facie argument rather than the current PR dance and it is – look at the TV ads Dominion is paying mucho money for and at the end it says “contact your legislators! Remember – this is a regulated monopoly using quasi govt powers (like eminent domain) to conduct business..

That’s why I asked if other regulated utility monopolies in other states do things like directly donate money to the same folks that are considering legislation and running advocacies ads on TV to contact legislators – and advocating to legislators – removing the SCC from some of it’s regulatory oversight… etc..

Dominion certainty has a vitally important role in literally maintaining the health and welfare of all who depend on electricity -no question about it – and they are a well-run and highly respected company – a leader in the industry…but I think they are overstepping in ways – not good for ratepayers, taxpayers.. and themselves and their investors… if the current SCC regime of regulation has become obsolete.. then lets’ deal with that in a meritorious way. Having the GA “direct” Dominion to build more solar and upgrade the grid – ….. geeze…

-

Eleven years ago the prospect of an unregulated monopoly electric company worried the General Assembly to the point that it forced Dominion back into a regulated environment. Legislation in 2013, 2014 and 2015 chipped away at it, and this bill completes the job – Governor Northam will sign a bill that gives Virginia totally unregulated monopoly utilities that are fully integrated, owning their own generation, free to earn and keep excess profits without limit, and fully insulated from any chance of competition (those bills are dying). The SCC will be a Potemkin Village. Jim is right, their credit and Wall Street ratings are going to improve substantially. What’s good for Dominion is good for Virginia.

There will be plenty of time to unpack this in the aftermath. As a soon to be ex-lobbyist, I will be completely free to do so. This is the not the General Assembly I first encountered in 1985. Those ladies and gentlemen would be very reluctant to ignore a chorus of uniform warnings from the SCC, the Consumer Counsel at the AG’s office, and every regulatory lawyer in the room who is not on the utility payroll. When they saw the Chamber of Commerce lining up with the most dedicated environmental advocates they would know for certain that the bumping noise they heard in the dark was not Santa Claus. (It is the ghost of Henry Howell actually…)

-

Poor, poor cash starved Dominion can somehow pay $3.34 per share in annual dividends, up 10% ….

https://seekingalpha.com/news/3318686-dominion-energy-increases-dividend-10-percent

Don’t buy their BS Jim.

-

Dominion Energy pays the dividends, not Dominion Energy Virginia, its regulated subsidiary. Obviously, DEV is a major contributors to the parent company’s earnings and cash flow, but it’s important to maintain a distinction.

What I have observed in the comments so far is people predisposed to dislike Dominion simply reiterating their distrust and dislike of Dominion — not contesting the facts and arguments that I laid out in the post. Clearly, Dominion’s arguments are self-interested. But please explain to me why they are B.S. If you can’t articulate why they are B.S., it’s hard to take your argument seriously.

-

It is important to note that the parent Dominion Resources can take money paid up to it by Dominion Virginia Energy (the utility) and invest in any business it wants, risky (purchasing a South Carolina utility with a bad nuclear generation program) or not (purchasing natural gas assets nationwide) with funds generated year after year by Virginia customers through rates that are set too high. In addition, through this legislation, it will fund additional infrastructure in Virginia, some of which is likely necessary and some of which may not be, without having to access the capital markets at all. The utility’s customers or ratepayers are thus transformed into unwilling and unpaid “investors” in the Company’s capital projects.

Remember that other provisions of the bill deem particular amounts of spending and particular types of generation projects to be “in the public interest” for a period of the next 10 years. Thus, the utility can build solar and wind generation projects whether it needs to or not, and will earn a return on this investment, irrespective of whether the dollars are deposited into base rates or collected through rate riders.

The rate riders themselves guarantee the return, dollar for dollar, of every dollar spent on the identified project whether it be a new gas-fired generation plant, a solar project, an energy efficiency project, or spending necessary to comply with environmental regulations, PLUS PROFIT (the return on equity). The utility has ZERO risk of undercollecting any of these funds, whether hurricanes hit the Commonewealth or whatever else you might think of.

The double-dip occurs because the ratepayer funded capital projects, paid for out of the confiscated “overearnings,” which is another word for customer overpayments of fair rates, will be placed into the company’s “rate base” and collected through base rates over the life of the project as if they had NOT been paid for at all. Usually in regulatory accounting the utility is not permitted to earn a return on capital contributed by customers. It’s not allowed to earn a return because it has made NO investment, it’s customers have. Usually, these are small items such as line extensions or a contractor paying to have service lines put underground in a new housing development. Here, we are talking about billions of dollars of unpaid investments over the next decade, not hundreds or thousands of dollars of contributions.

And, while these “in the public interest” projects remain in base rates, the returns they earn will soak up the earnings that would otherwise be counted toward the theoretical customer refunds that the law otherwise requires to be repaid, in part mind you, not in whole, to customers.

That’s a double dip. Pay me this year through unrefunded overearnings and pay me over the life of the project through future uncounted overearnings. I think the legislators pretty much know how this is going to work.

But, as Upton Sinclair so memorably said “”It is difficult to get a man to understand something, when his salary depends upon his not understanding it!”

-

In this case Jim I think I agreed with your basic argument that Dominion was seeking to increase its revenue and margins in order to lower its risk and thereby lower its capital costs. I just don’t believe it is doing so to benefit its customers and I think the customers are taking on the risk instead.

https://www.youtube.com/watch?v=_Gix0iHiUck&feature=youtu.be

I do love Kim Pate of the SCC’s explanation of how…

-

-

-

And when they’re not busy using their cash to jack up the dividend to shareholders they are using the cash to buy back great blocks of their shares …

https://www.cnbc.com/id/19476091

Dominion borrows and charges the ratepayers interest so they can use the free cash flow from ratepayers to enrich the shareholders through huge dividend increases and share buybacks. All done with the complicity of The Imperial Clown Show in Richmond.

Don’t buy their BS Jim. But you might want to buy their stock. After all, the profits are stolen from the citizens of Virginia so you could at least recoup your share of the heist.

-

For the record, Dominion closed yesterday at $73.31. Their freshly raised dividend of $3.34 per share per year gives the stock a staggering dividend yield of 4.6%. That’s a mighty fat payout for people holding equity in a monopoly which has purchased the legislature that regulates it.

-

By itself, dividend yield is meaningless as far as understanding Dominion’s profitability. Yield must be viewed in the context of cash flow, return on equity, leverage, price-earnings multiples, and a host of other indicators of financial performance and investor confidence.

More to the point, dividends reflect the financial performance and investor evaluation of the parent company, not the regulated utility. Dominion has many assets other than Dominion Virginia Energy.

That said, it would be interesting to take a look at the profitability of Dominion Energy Virginia, and it would be interesting to know how that compares to the financial performance of other regulated utilities.

This would be the starting point of any analysis: http://www.scc.virginia.gov/comm/reports/2017_veurcomb.pdf

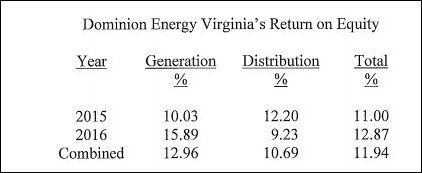

Go the bottom of Page 5 and start reading.“DEV’s analysis reflects a combined base rate generation and distribution earned ROE for calendar year 2016 of 12.87% on a regulatory accounting basis. Separately, the 2016 generation and distribution earned ROEs were 15.89% and 9.23%, respectively. The combined generation and distribution earned ROE of 12.87% exceeds the 9.60% ROE approved by the Commission for DEV’s RACs during 201614 by 3.27 percentage points, or approximately $251.9 million in revenues, and exceeds the 10.00% ROE approved by the Commission in DEV’s last biennial reviewl by 2.87%, or approximately $221.1 million in revenues.”

Or, in tabular form:

https://www.baconsrebellion.com/wp-content/uploads/2018/02/dominion_earnings.jpg-

Your contention, if I understand it correctly, is that Dominion should keep the overpayment so they don’t have to engage in excessive borrowing which could raise their interest rates which get passed along to ratepayers. The crux of that argument is that Dominion lacks the cash to self finance these projects. My point is that they are pouring cash into share buybacks and dividend payments. These uses of cash reward the shareholders. They also effectively penalize the ratepayers since the money that could be used to self-finance is used instead to buyback shares and payout what I consider to be an excessive dividend.

You started to peel back the onion but you didn’t peel far enough. Dominion is a cash cow. If they decide to borrow instead of self-finance that’s a decision they make regardless of their ability to self-finance. They don’t need to keep the over-payments to avoid borrowing. They could stop raising their dividend by 10% a year. They could reduce their dividend. They could use the cash from the regulated company for capital expenditures instead of dividend payout.

-

-

-

The part that concerns me is:

8. In any triennial review proceeding, for the purposes of reviewing earnings on the utility’s rates for generation and distribution services, the following utility generation and distribution costs not proposed for recovery under any other subdivision of this subsection, as recorded per books by the utility for financial reporting purposes and accrued against income, shall be attributed to the test periods under review and deemed fully recovered in the period recorded: ……. costs associated with projects necessary to comply with state or federal environmental laws, regulations, or judicial or administrative orders relating to coal combustion by-product management that the utility does not petition to recover through a rate adjustment clause pursuant to subdivision ….

Does this mean coal ash remediation at the expense of ratepayer refunds, ensuring the shareholders don’t pay for it?

-

Liberals should be happy…Dominion is committing to intentionally keep profit margins high, which increases our elec bills and makes renewables look more competitive. Plus Dominion is committing to spend a lot of money on solar and grid enhancements.

Of course Dominion really just wants to build anything, because they get paid back from us rate payers including profits. Elected officials like it because it creates jobs and money flow, and is essentially the one industry state gov’t can run by themselves and force to locate in Virginia and create jobs here.

All I can say is, it is better than the old days when coal-fired power plants was the main project utilities and states wanted to push through like this.

-

Argh. I neglected to read to the bottom of the Wall Street Journal article that I quoted in the post. Had I done so, I would have encountered this:

Earlier last month, S&P changed its outlook for Dominion Energy Inc., a Virginia-based gas-and-power company, to negative from stable.

The soured outlook means that there is at least a one in three chance that the company’s current triple B+ rating will be downgraded within the next two years…. A lower credit rating can result in higher interest rates, and therefore higher payments on new or refinanced debt, though broader bond market forces can temper that impact.

A spokesman for Dominion declined to comment.

-

This is the holding company the WSJ is talking about, not the Virginia-regulated retail subsidiary. These MUST be looked at separately. DE is buying SCG&E and at the holding company level that exposes it to substantial new risks, such as that unfinished new nuke. Whether DVE [I called it DVP earlier, must update my acronym!] or the federal income tax reduction contributes whatever to S&P’s downgrading in credit quality, or not, cannot be determined from this little article.

This simply underscores the larger point: the SCC is the only Virginia body with the expertise and the patience and the time to sort through all this. They should not have to do so with their regulatory hands tied. Moreover the GA fails miserably on all fronts (expertise, patience, time) as an alternative regulator.

The FERC does something similar with respect to transmission rates — it would be interesting to compare the “cost of service” results.

-

-

Obviously, there are two types of risk for utilities (and every other business, for that matter): Financial Risk and Business Risk. With their high debt levels, utilities have generally had a higher financial risk than companies with less debt. But if Dominion gets to convert consumer refunds to grid investments, it gets some zero cost capital, which, in turn, reduces its financial risk and should lower its cost of capital and allowed rate of return.

I’d say Dominion faces more business risk now than a few years ago. It is facing competition in the generating business; needs to harden its distribution grid; and has a lot of sunk investment in fossil fuels generating plants. This increased business risk should raise its cost of capital. On the other hand, it strikes me that much of its older generating capacity is likely completely or largely depreciated. That reduces its risk and cost of capital some.

I’d like to see a VSCC review (even using a two-year test period) of Dominion’s cost of capital and proper earnings level.

-

“But if Dominion gets to convert consumer refunds to grid investments, it gets some zero cost capital, which, in turn, reduces its financial risk and should lower its cost of capital and allowed rate of return.”

I’m assuming that some percentage of the cash Dominion uses to pay dividends comes from cash flow out of the regulated company. Last year Dominion raised its already healthy dividend by 10%. If they would have left it flat couldn’t they have financed more of the regulated company’s capital needs with the regulated company’s cash flow? In that case, couldn’t they have made the refunds to the ratepayers, made the capital investments and kept current debt levels? Why would a company facing financial risks already paying a healthy dividend raise that dividend by 10% in a single year?

-

-

There is a lot of BS being thrown out here. JIm, your post makes the point that DOM may be hurt by the reduction in federal corporate tax, because, ““If [cash flow] is going to be smaller, to us, the financial risk has gone up,” the Journal quotes Toby Shea, a senior credit officer at Moody’s, as saying.” And you provide a WSJ citation which says on this subject, in its entirety: “The steady stream of customer bill payments underpins utilities’ credit ratings, which in turn dictate their cost of debt.” That is ALL the explanation provided by the WSJ. At one level that’s a truism (of course cash flow affects credit ratings); at another that is total BS (it is far from the most significant factor and may be negligible).

Have you ever heard the phrase “cash cow”? That’s what DVP is, to the parent. Yes it’s true, without a high level of cash flow the utility might have to increase its working capital, which would show up as a cost in the next base rate proceeding (sometime in the next decade?). But wait: what effect on cash flow are we even talking about? First, how much federal income tax does poor old DVP actually pay? Hell, it’s been reported here before that DVP actually generates tax losses for the parent Dominion Energy. If so the tax bill would hurt DVP only insofar as those accumulated tax losses would get consumed less rapidly by it or its parent company. I don’t know for a fact that was or still is the case, but that sure does affect the size of any potential tax rebate to DVP customers and any consequent reduction in regulated cash flow.

Then there’s the broader question of whether any of this setting-aside of potential refunds for specific “new” investments like solving the ash disposal problem and building more utility-scale solar or “modernizing the grid” aren’t anything but the usual verbal flim-flam associated with cherry-picking for discussion just a few of the regular, ordinary, normal-course-of-business expenses that any regulated utility has to deal with over the years! A proper regulatory scheme simply nets all these out periodically in a base rate proceeding unencumbered by RAC-set-asides and politically-off-limits costs where the Commission looks at everything under its jurisdiction all at once and fixes a single set of rates that reflect that and adjusts those rates if, and only if, the utility demonstrates subsequently that its total cost of service has increased. Get rid of the RACs — except, maybe, the fuel rider. Get rid of the pigeonholed expenses with their dedicated funding, carefully calibrated so you don’t get to see the big picture. GEt rid of DOM continuing to rate-base new generation that in fact operates in a competitive wholesale market, not dedicated to DVP ratepayers. This is an obscene way to regulate the largest public utility in the State.

-

Thank you AC. I did not scroll down to your comment before I responded to Jim above. This is exactly how I feel.

The SCC should be reviewing utility proposals and deciding which is in the public interest and should be funded. Rates should reflect all costs of providing service, plus allowing the utility the opportunity to EARN its fair rate of return, not guaranteeing it.

-

A few years ago I was in the audience as Virginia Electric & Power Co. wrapped up a several-days-long base rate case with dozens of witnesses and countless reams of paper filed. The Commission closed the hearings late one morning, took a lunch break, then reconvened after lunch when, to the astonishment of some, Chairman Catterall announced from the bench the Commission’s decision on the overall revenue requirement and directed the Company to file revised rates accordingly. No opinion; no discussion of the contested items in writing; that was it. THAT was utility regulation in the 60s and early 70s.

It is not surprising that the 1970s brought about a steady stream of GA regulatory requirements, including all the mandatory annual rate of return calculations and fuel rate review provisions and annual base rate review and integrated-resource-plan requirements and specified rate of return methodology and such, even the requirement that the Commission issue its written opinions prior to the filing of an appeal. After all these were the Henry Howell “Keep the Big Boys Honest” years!

But I tend to the view that the GA got way too far down into the weeds with its late-90s restructuring bill to accommodate unbundling and “retail access.” And then went off the deep end with its 2007 “reversal” of those provisions (which wasn’t a reversal at all, but a turn to a new rate methodology like nothing Virginia ever tried before). And the subsequent manipulations of the 2007 framework (with its RACs and specified multi-year review and freeze periods) have been appalling.

I do think the SCC staff contributed to this hostile atmosphere. The Commission tried to automate the ratemaking process with everything filled out in reams of forms and the bottom line an automatic consequence. Staff became very unresponsive to special and changing circumstances and ratemaking adjustments in my opinion. But it doesn’t work like that; the ratemaking process is (and ought to be) a politically-informed bottom-line judgment that should remain simultaneously straightforward and opaque, not a mere spreadsheet calculation. Not that we should bring back Judge Catterall’s ways; but he had a point.

Staff also became particularly hostile to the PJM wholesale energy marketplace with its FERC-approved marginal cost pricing regime, which the SCC never understood as a matter of economic theory. Its 2007 comments on the PJM markets created a lot of mistrust and unnecessary misunderstanding, both at the Commission and in the GA, and also in PJM and OPSI circles. Now, over a decade later, the SCC would hopefully say better things about DVE relying on the wholesale marketplace for purchases to a greater extent, but that mistrust contributed substantially to the Commission’s support for Dominion continuing to rate-base new generation construction, which I still think is a fundamentally wrongheaded feature of Dominion’s current rates.

-

Only a ‘few years” ago, AC? Judge Catterall last sat on the Commission in 1973!

I am intrigued by your comments on the SCC staff and its role in engendering hostilities between the Commission and the Assembly. I wonder if you could illustrate your statement “Staff became unresponsive to special and changing circumstances” with an example or two?

I have only been an observer of the SCC since the 1990s and I cannot bring such an example to mind during that time frame.

Thanks.

-

Once upon a time I worked for Potomac Electric Power Co., dealing with the Virginia Commission on behalf of Pepco. Around 1986 Pepco sold its Virginia service territory (a small retail area in Arlington County’s Rosslyn neighborhood, plus the Pentagon, a non-jurisdictional customer) to Virginia Power in part to simplify its retail regulatory burden, because Pepco had to file all the same schedules and forms and reports with the SCC and go through the same process for base rate and fuel rate changes that Vepco did, all for just a few thousand dollars of jurisdictional sales. Our submissions, which reflected our membership in PJM and heavy participation in the Pool’s “split the savings” energy market and our bulk purchases from Ohio Edison, were required to fit a Staff template designed for stand-alone Virginia Power, and our requests for more reporting flexibility (even when we joined with Apco in asking) were generally ignorerd. Later, Pepco sold its generation and bought Delmarva Power, which also had a small Virginia service territory on the Eastern Shore, and again, the SCC Staff seemed to Conectiv’s regulatory folks to be inflexible and/or hostile to the different energy-market environment that existed in PJM.

This was again illustrated by the SCC’s reaction when Dominion was compelled by the FERC to join an ISO and chose to join PJM. Dominion came under PJM operational control in 2005 but the SCC (based on its Staff’s report) cited the failure of competition in the PJM marketplace as the reason why Virginia Power should, essentially, ignore the PJM energy and capacity markets and build its own generation as though it were still an isolated, vertically-integrated utility. And the SCC so recommended to the GA. I was not there in the GA, of course, but those who were tell me that the SCC had a large hand in causing the policy reversal in 2007 that un-did retail access and caused Dominion to resume new generation construction not for unregulated competitive purposes but for Virginia customers and rate-basing.

The SCC did not believe that PJM worked well enough to trust it. See, for example, “[T]his Commission remains unable to independently warrant that PJM’s competitive wholesale electricity markets are effectively competitive.” https://www.scc.virginia.gov/comm/reports/2006_part3.pdf , at pages 3-5 (numbered pages 2-4), et seq. (2006) which was based on this: “”Electric market characteristics suggest that the market structure is not a robustly competitive one, as was hoped when restructuring began. . . . Coordinated interaction and tacit collusion among suppliers also could have particular relevance for electric markets. . . . Studies have shown that anti-competitive bidding strategies are possible and the 2000-2001 western power crisis demonstrated that it can and does happen. Given the fact that such strategies have been shown to be possible and successful, it is likely that suppliers are currently using strategic bidding techniques and witholding strategies to raise the price, strategies that would be less effective in a more competitive market.” https://www.scc.virginia.gov/comm/reports/2006_rose_1.pdf , at 6-7 (2006).

Ken Rose’s piece, which was written several years after the California ENRON scandals and shortly after Dominion joined the PJM operating region and market under pressure from FERC to do so, was considered quite the “hatchet job” in PJM circles and assumed to have been commissioned by SCC staff who were hostile to FERC’s “independent system operator” initiative and to PJM generally. You may well ask, why the hostility? Unfortunately PJM (whose marketplace has now grown to about 3-4 times larger than it was then and is pretty clearly competitive) had operated next door to Dominion as a power pool since the 1920s and there was a history of contentious rivalry rather than cooperation between Dominion and PJM. Also, I think there’s a whiff of northern versus southern differences in approach, here: to this day the electric utilities in the southeastern states (except VA) are only nominally members of ISOs, with vestigial wholesale markets organized mainly around the old holding company networks like Southern Co’s subsidiaries, contrasted with the “strong” ISOs in the east: PJM, NYISO, ISONE, MISO, and the Texas grid. And as far as the politics was concerned, the notion of States rights and resentment over FERC’s ISO initiative also resonated in the SCC and in Virginia’s GA. It’s true, FERC forced Virginia Power to join PJM (although originally, FERC’s pressure was for VaPwr to choose whether to join PJM, or MISO, or participate in forming a new southern ISO with one or more NC and SC companies, but VaPwr rejected those other options).

How much of this SCC hostility might have come ultimately from Dominion? I don’t know enough to say. I do know that the Dominion folks I worked with over the years were outstanding professionals with a good understanding of wholesale energy markets, and viewed the occasional policy dictate from on high as driven by politics that was beyond them.

-

I did reply to you yesterday but it’s still stuck in “awaiting moderation” limbo because it contains a couple of links. But meanwhile, this 3-part TD article last year was a good one and I thought accurately reflected the origins, if not the source, of the SCC-GA tensions from the 90s. I happen to think that Tom Farrell was right the first time, that the SCC was wrong to reject DOM’s spinoff and de-regulation of its generation, and that the “DOM dodged the bullet” view TF expressed later was wrong; but also, that Hully Moore was right (if not politically wise) to oppose the GA’s regulatory interference so emphatically, which interference has had consequences for the Legislature we are just now confronting. See:

DOMINION RULES, by MICHAEL MARTZ, Richmond Times-Dispatch Oct 13, 2017 http://www.richmond.com/news/special-report/dominion/attempted-coup/article_9473e652-af53-11e7-86ed-87a90399973c.html -

Thanks for your responses, AC. Like I said before, I’m not in a position to comment on things that occurred prior to the early 1990s, such as the regulation of Potomac Edison when it served in Virginia, but I do believe that Delmarva Power & Light Company was an original member of PJM beginning in 1927 and had been subject to regulation by the SCC continually since that time, until it sold off its service territory in the mid-00s. I’m not entirely surprised to find that after its acquisition by the parent of Pepco, there might have been some tensions between the SCC staff and Connectiv staff.

I disagree with you that FERC compelled Dominion to join an RTO. Code of Virginia Section 56-579, enacted as part of the 1999 restructuring regulation, is what obligated all Virginia investor owned utilities to “join or establish” a regional transmission entity. If you recall, Dominion and Appalachian (through its parent, American Electric Power) tried for several years, with FERC’s putative encouragement, to “establish” an RTO that would have been called “The Alliance.” Ultimately, the huge utility Commonwealth Edison, now called Exelon, which had acquired several utility systems on the east coast and which would have to have transported its nuclear generation in Illinois through The Alliance to these newly acquired systems, convinced FERC to disapprove that grouping and then sued both the Virginia and Kentucky commissions to compel them to approve the admission of Virginia Power and the AEP affiliates in Virginia (Apco) and Kentucky (Kentucky Power) to join PJM. Shortly thereafter, FERC’s then-Chair, Betsy Moler, found post government employment at, well, take a guess.

The litigation dragged on for nearly a year before the FERC back in the early 2000s and was eventually mooted out when both state Commissions approved the enrollments under their respective state laws.

PJM to this day has an Independent Market Monitor. To my knowledge, the IMM has NEVER determined the PJM markets to be competitive. Indeed, PJM is effectively just another regulatory agency, with volumes of onerous rules and regulations that it enforces, or that FERC enforces, or that the IMM enforces to interdict anti-competitive bidding strategies and other types of market power. Among those rules are capacity obligations that require each member to either construct or contract for capacity sufficient to serve its load plus a reserve margin.

You may or may not have been present around the conception of the so-called Re-regulation Act of 2007 to hear the wailing and lamentation of the lawmakers decrying the “importation” of power from PJM (though through their earlier wisdom they had compelled our utilities to join up with an RTO somewhere) and hence the passage of unnecessary “sweeteners” to incent construction of new generation in the Commonwealth, including a coal fired plant in the coalfield region of Virginia as an economic development project. I really don’t see how that bill, also written by Dominion attorneys and lobbyists, can be laid at the foot of the SCC staff, but maybe Steve Haner has some insights on that point.

-

-

-

-

-

Just want to say ,I am NOT predisposed against Dominion at all.

It is in everyone’s interests that Dominion be – a thriving company.

But they should NOT be driving the regulatory bus instead of the SCC.

If regulations need to be revised to reflect the state of the industry – then do it.

If regulators needs to evolve on the same basis – do it.

But Dominion should not be deciding what the regulatory regime should be.

I had asked earlier – is what Dominon is pursuing in Va – something that is fairly standard throughout the other states or Dominion way out in front?

In no way, shape or form should Dominion be writing legislation and especially legislation that defines what the SCC role is or is not.

If things need to change – fine -make that prima facie case but what this feels like is that Dominion does not want to be regulated anymore and the argument is that the industry “has changed” and the SCC needs to be a rubber stamp type agency.

I’m not buying it.

-

Larry, at no time in any discussion has Dominion stated that this “customer credit reinvestment offset” is modeled on any other state’s regulatory scheme. IMHO, as I’ve stated, it is a cover for several more steps toward deregulation – which is the situation in some states. Certainly if the SCC cannot order rate cuts or refunds (due to the many new opportunities for the utility to manipulate its earnings) then setting an official return on equity is an exercise in futility – they still keep it all.

-

-

The process is just wrong. Dominion should not be writing legislation and contributing money to the same folks considering the legislation.

You don’t need to be an enemy of Dominion to see this. You can be a friend of Dominion and see the potential of bad outcomes.

If we as a state – cannot see that – and we’re going to stand by and watch the process work like that – then we need to be ashamed… this is bad. We point fingers at places like Chicago and New Jersey for their conflicted governance but this is the pot calling the kettle black.

{kind=link}

Leave a Reply

You must be logged in to post a comment.