Ten years ago the Lehman Brothers debacle precipitated the financial meltdown we associate with the Great Recession, and the financial media are full of retrospectives. A key question is what lessons we learned from the epic failure. The main conclusion drawn, according to Daniel J. Arbess in the Wall Street Journal today, appears to be that the way to dig out of a debt-fueled financial crisis is to pile on more debt. But that doubles down on the original problem, he warns:

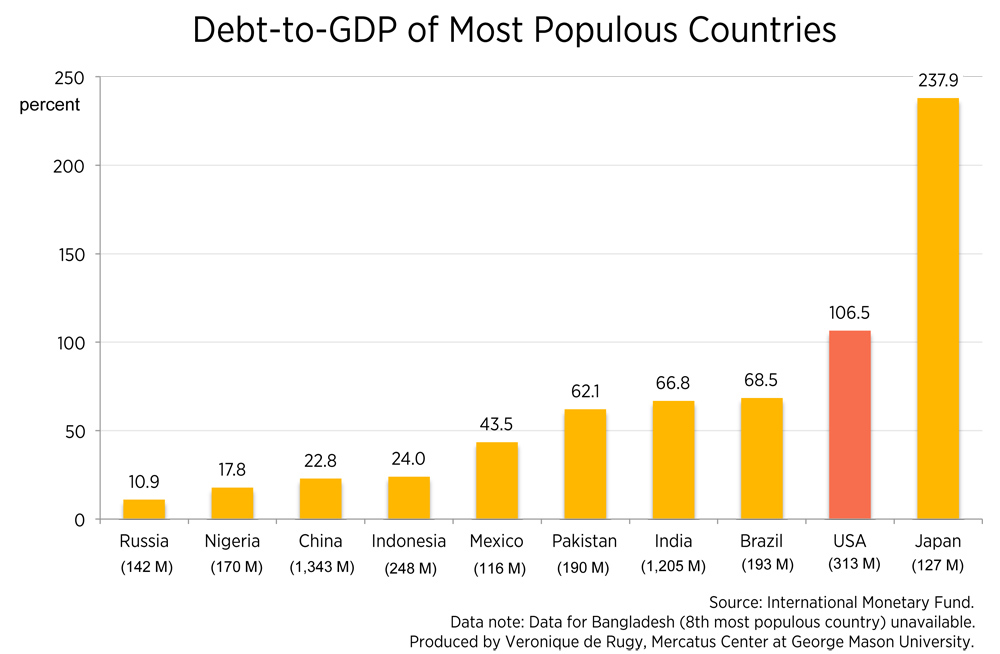

In the past decade, total global debt (sovereign, corporate and household) has spiked nearly 75%. This includes a doubling of sovereign debt, from $29 trillion to $60 trillion, according to a recent McKinsey report. Total corporate debt increased by 78% over the same decade, to $66 trillion. Bank loan volumes have been stable, although low-quality “covenant lite” loans have dominated. Bond markets have filled in, with nonfinancial bonds outstanding up 172%, from $4.3 trillion to $11.7 trillion. McKinsey says 40% of U.S. companies are rated one notch above “junk” or lower, and the Bank for International Settlements estimates 10% of legacy companies in the developed world are “zombies,” meaning earnings before interest and taxes don’t cover interest expenses.

This is what zero interest rates and quantitative easing have wrought — more debt and lower credit quality. … Higher rates are coming, possibly heralding a tsunami of credit defaults.

As the Federal Reserve and the European Central Bank slowly dial back quantitative easing, interest rates will rise, stressing debt-laden governments, corporations and households. We are already seeing the effects in Turkey, Venezuela, Argentina and other developing nations as higher U.S. interest rates push the value of the dollar higher. Defaults in developing countries will be transmitted to the developed world in ways foreseeable and unforeseeable. The financial media have remarked upon the massive exposure of Spanish banks to the Turkish economy, for instance, which could prove problematic for the larger Spanish economy, the 13th largest in the world. But global markets are so complex and intertwined that defaults can spread as unpredictably and explosively as the sub-prime mortgage loan crisis in the U.S. did ten years ago via financial innovations that have so far eluded the notice of media and regulators.

What’s it to us? That’s all fine and good for bond traders and hedge fund managers, you say, but what difference does it make to Virginia? It matters because Virginia is part of the global economy and global financial system, and what happens elsewhere will impact us. The policies we pursue at the level of state/local government can make us more vulnerable to, or more resilient in the face of, the next financial crisis.

To be sure, the Commonwealth is nowhere as vulnerable as, say, Puerto Rico was before it declared bankruptcy, or as Illinois and Chicago now are. We have a AAA credit rating, we balance our budget with only a modicum of chiseling, and we pay our bills on time. But the bond rating of the Commonwealth does not tell us anything about the indebtedness of our local governments, our universities, our hospitals, our quasi-government organizations, our economic development authorities, our housing authorities and all the other bond-issuing entities in the state. No one has toted up all those numbers.

We continually discover things we didn’t know before. While Virginia’s $20 billion or so in unfunded pension liabilities are well known, only recently has our attention been drawn to the $3.5 billion in pension liabilities at the Washington Metropolitan Area Transit Authority (WMATA), which operates Northern Virginia’s heavy rail mass transit system and much of its bus system. As the Government Accountability Organization concluded, “Due to their relative size, proportion of retirees compared to active members, and investment decisions, these pension plans pose significant risk to WMATA’s financial operations, yet WMATA has not fully assessed the risks.”

How many other WMATAs are out there?

The Metropolitan Washington Airports Authority (MWAA) comprehensive annual financial report indicates that the authority’s two pension plans were fully funded as of Dec. 21, 2017. The General Employees Retirement Plan was seemingly in great shape with assets amounting to 105% of pension liabilities. Great news! But dig into the assumptions, and we see that the pension plan projects a 7.5% annualized investment rate of return. Many actuaries are saying now that a 7% or 6.5% rate is more realistic.

Similarly, the Ports of Virginia reported an unfunded pension liability of only $8.9 million as of June 30, 2016, an improvement over the previous year. The pension was about 91% funded. The ports assumed a 7% investment rate of return, somewhat more conservative than MWAA’s assumption.

MWAA and the Ports of Virginia are two of the largest quasi-governmental business entities in Virginia, and it is reassuring to see that they have their pensions under reasonably good control. But there are dozens if not hundreds of other bond-issuing entities in the Commonwealth. After the Petersburg fiscal meltdown, the General Assembly began watching for early warning signs in Virginia’s local governments, but there are dozens if not hundreds of other entities that issue bonds and borrow money. The federal government conducts “stress” tests on too-big-to-fail banks to see how they would hold up under adverse economic circumstances. Is anyone conducting stress tests for Virginia’s public and quasi-public entities? Not very likely.

The bottom line: Another global debt crisis is inevitable, the only questions are when it happens and how the damage ricochets throughout the global economy. How vulnerable is Virginia? We really don’t know. To be forewarned, as the saying goes, is to be forearmed. We are neither.

{kind=link}

Leave a Reply

You must be logged in to post a comment.