Consumer spending is a driving force behind the U.S. economy, accounting for about 70% of economic activity. When consumers borrow, they stimulate economic growth. When they stop borrowing, the economy retrenches. Thus, when analyzing the prospects for the nation’s economy, economists take into consideration the size of the consumer’s debt load. All other things being equal, a debt load that is high by historical standards suggests that consumers have less room to grow the economy by borrowing (although the consumer economy still can grow when people back to work, get better paying jobs, or benefit from tax cuts).

Consumer spending is a driving force behind the U.S. economy, accounting for about 70% of economic activity. When consumers borrow, they stimulate economic growth. When they stop borrowing, the economy retrenches. Thus, when analyzing the prospects for the nation’s economy, economists take into consideration the size of the consumer’s debt load. All other things being equal, a debt load that is high by historical standards suggests that consumers have less room to grow the economy by borrowing (although the consumer economy still can grow when people back to work, get better paying jobs, or benefit from tax cuts).

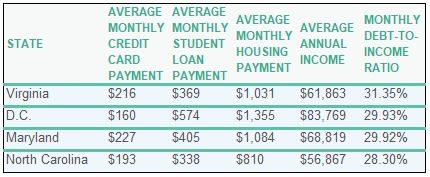

Compared to other states, Virginia’s consumers are among the more heavily indebted in the nation. Indeed, comparing payments for credit cards, student loans, and housing as a percentage of annual income, Virginians’ indebtedness is sixth highest in the country, according to Credible, a consumer finance website.

Virginia has enough economic troubles as it is, ranging from dependence upon federal spending to infrastructure issues to undeveloped innovation ecosystems. High consumer debt is icing on the cake.

For what it’s worth, Credible doesn’t provide a complete picture. The numbers don’t include auto-financing debt, a significant contributor to consumer debt. Maybe the consumer picture in Virginia isn’t as bad as it appears…. Or maybe it’s worse.

Meanwhile, there’s this news: Nine years of central bank stimulus and debt-bingeing around the world has made the U.S. and other economies more vulnerable than ever to a rise in interest rates, says William White, the Swiss-based head of the OECD’s review board and ex-chief economist for the Bank for International Settlements. “Market indicators right now look very similar to what we saw before the Lehman crisis, but the lesson has somehow been forgotten,” he says.

The edifice of inflated equity and asset markets is built on the premise that interest rates will remain pinned to the floor. The latest stability report by the US Treasury’s Office of Financial Research (OFR) warned that a 100 basis point rate rise would slash $1.2 trillion of value from the Barclays US Aggregate Bond Index, with further losses once junk bonds, fixed-rate mortgages, and derivatives are included. It said losses could dwarf the “bond massacre” that bankrupted Orange County California in 1994 – and detonated Mexico’s Tequila Crisis. …

The global fall-out from such a shock could be violent. Credit in dollars beyond US jurisdiction has risen fivefold in 15 years to over $10 trillion. “This is a very big number. As soon as the world gets into trouble, a lot of people are going to have trouble servicing that dollar debt,” said Prof White. The offshore dollar funding markets would dry up, triggering a liquidity squeeze. Borrowers would suffer the double shock of a rising dollar, and rising rates. …

Central banks are now caught in a ‘debt trap’. They cannot keep holding rates near zero as global inflation pressures build because that will lead to an even more perilous financial bubble, but they cannot easily raise rates either because it risks blowing up the system. “It is frankly scary,” he said.

Recessions are painful but cleansing. Economies need small but regular downturns to wring out speculative excess and maintain long-term stability. The U.S. is enjoying a burst of stronger economic growth this year thanks to tax cuts and a rollback of regulations, but the business cycle is one of the longest-running in U.S. history. It can’t go on forever, and it won’t.

I know my warnings must be tiresome. I raised the same alarm when I wrote “Boomergeddon” back in 2010, and look where we are now. The economy seems just fine…. just like it did before every big catastrophic market meltdown.