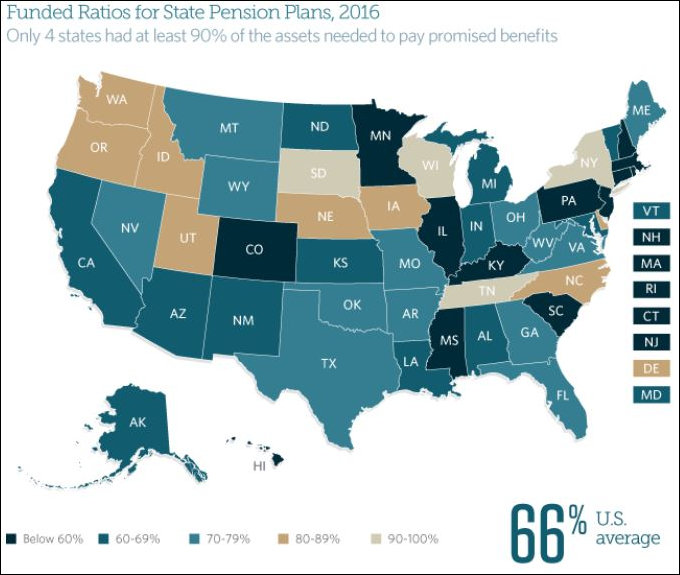

Map credit: Pew Charitable Trusts

Another year, and another analysis by the Pew Charitable Trusts on the deteriorating condition of U.S. states’ public employee pension plans. Drawing on data from 2016, Pew concludes that despite scattered actions by the 50 states to shore up their pensions, the funding gap only got worse.

In 2016, the state pension funds in this study cumulatively reported a $1.4 trillion deficit—representing a $295 billion jump from 2015 and the 15th annual increase in pension debt since 2000. Overall, state plans disclosed assets of just $2.6 trillion to cover total pension liabilities of $4 trillion.

There is considerable variability between the states, however. The funding ratio (assets as a percentage of liabilities) ranges from 99% for Wisconsin, which is in fine shape, to 31% for Kentucky and New Jersey, which are in deep doo-doo. The national average is 66%. Virginia is in modestly better condition than the national average with a funding ratio of 72%. Our net pension liability in 2016 was “only” $25.3 billion.

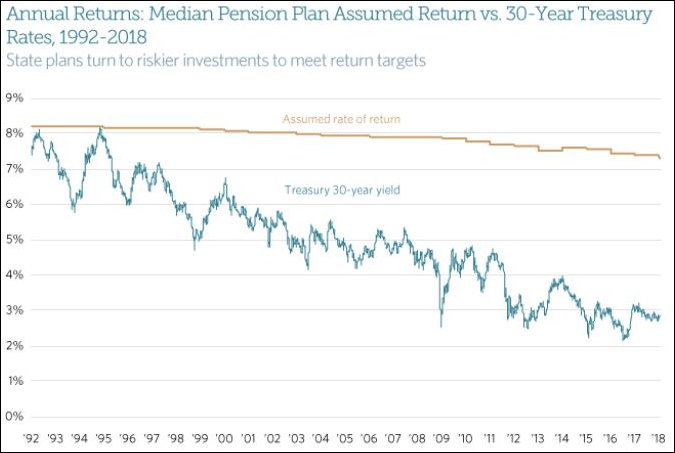

Admittedly, 2016 was a tough year in which state pension plans generated a mere 1% return on their investments, significantly short of the 7% to 7.5% returns that most plans are predicated upon. (Virginia assumes a 7% return.) Investment performance shined last year, which could improve 2017 performance when Pew gets around to calculating it a year from now.

However, investment returns are likely to become more volatile, Pew notes. As the gap between the return on 30-year Treasury bonds and equity returns has widened over the past two decades, pensions have shifted assets to riskier investments in the hope of generating a bigger payback.

The share of public funds’ investments in stocks, private equity, and other risky assets has increased by over 30 percentage points since 1990—to over 70 percent of the portfolio of state pension plans. As a result, pension plan investment performance now tracks equity returns more closely than bond returns.

That’s great news when the stock market goes up, as it did last year. But when interest rates rise and market multiples shrink, as is happening this year, pension funds are vulnerable to setbacks in stocks, private equities, and interest-sensitive real estate investments.

Pew has developed a set of analytical tools that allow a more penetrating look at a state’s pension posture. One of those is “net amortization as a percentage of payroll for each state.”

There are two ways for states to increase the assets in their pension plans. One is to earn a higher rate of return on its investment portfolio. The other is to contribute more (in employee contributions and government contributions) into the plan.

With the “net amortization” metric, Pew assumes that the pension plan earns the assumed rate of return (even though that assumption isn’t always justified). The idea is to determine whether state/employee contributions are putting in enough to cover new benefits earned that year. States the study: “Plans that consistently fall short of this benchmark can expect to see the gap between the liability for promised benefits and available funds grow over time.”

Some states are doing a horrible job — Kentucky, New Jersey, and Illinois are ticking time bombs. Kentucky paid in only 41% of its benchmark in 2016, and New Jersey only 33%. The national average was 88%. Virginia looked pretty good by comparison, paying in 101% and whittling down its net liability by one whole percentage point!

Pew also looks at what it calls “operating cash flow” — the difference between financial outflows (primarily benefit payments) and employer/employee contributions expressed as a percentage of assets at the beginning of the year. “A plan with an operating cash flow ratio of 3 percent, for example, would need to achieve investment returns of at least 3 percent that year to keep assets from dropping.”

In total, state pension plans paid out $214 billion in pension benefits in 2016, and took in $37 billion in employee contributions and $93 billion from employers. Dividing the cash flow by the total asset value of $2.6 trillion results in an average operating cash flow ratio of 3.2 percent for states in 2016.

New Jersey and Kentucky were the worst performers, with negative cash flow exceeding 4%. Kansas fared the best. Indeed it was the only state in the country to show a positive cash flow. By this metric, Virginia was the ninth best performer — we had a negative cash flow ratio of only 1.8%.

Bacon’s bottom line: State pensions are in bad shape, and they’re getting worse. Virginia is no exception to the broader trend. If there’s any consolation, several other states are likely to hit the wall before we are. A pension crisis looks almost unavoidable for Kentucky, New Jersey, and Illinois — and by “crisis,” I mean a default on its pension obligations. We’re talking Boomergeddon, baby.

Hopefully, the calamities of others will serve as a notice to Virginia that our pension problems are real. Given enough warning, maybe we can get our act together.