Source: VRS Report to JLARC

State and local employees, like many of their peers in the private sector, are declining in droves to contribute to their own retirement plans, despite the availability of matching funds, a.k.a. free money which compounds for decades.

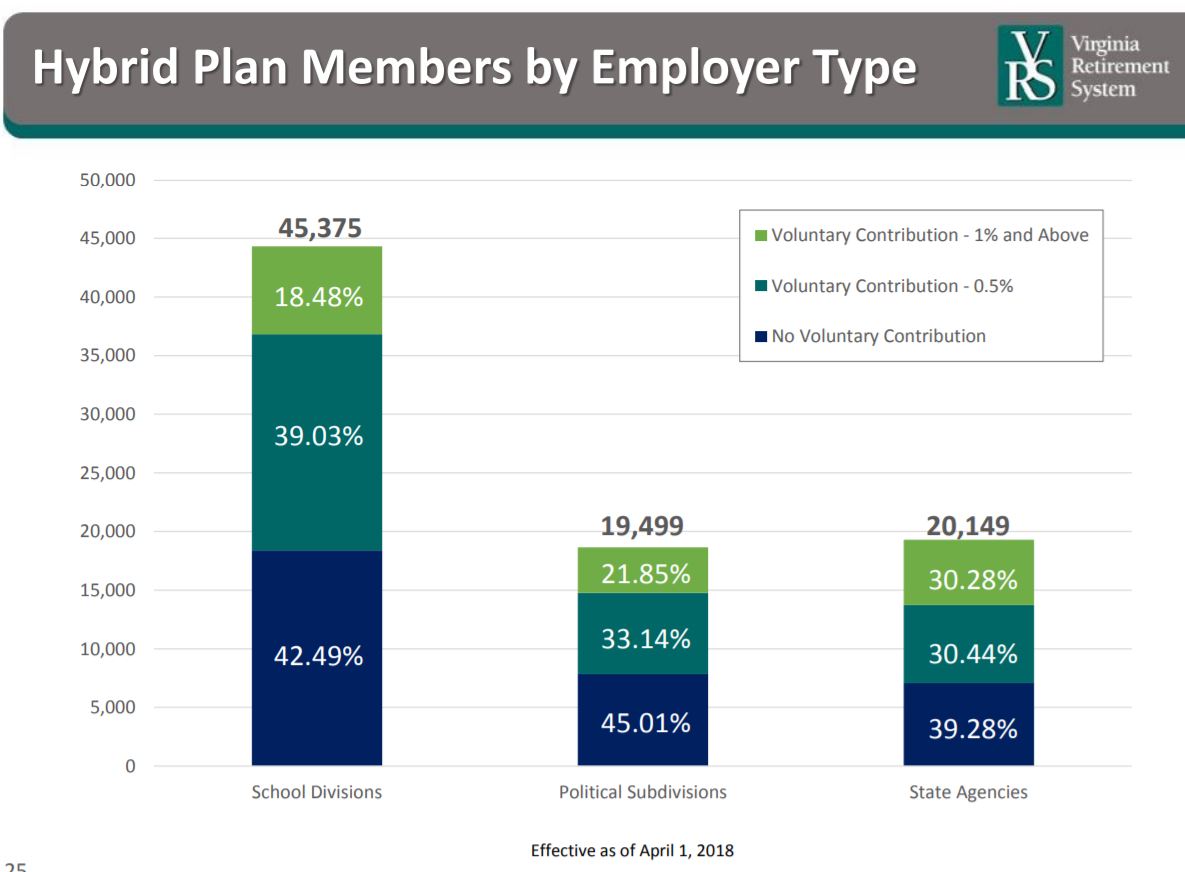

The Virginia Retirement System has been putting new hires into a hybrid retirement plan that combines a defined benefit with a defined contribution plan which depends on employee contributions. More than 85,000 active workers are now part of the hybrid plan, but only 18 percent of those are socking away the maximum 4 percent of their pay, which is matched with another 2.5 percent by the state.

Of the rest, 42 percent are contributing nothing, and 36 percent are contributing only one-half of one percent, or $50 per $10,000. Most of those are apparently doing so because the state automatically escalated all contribution rates by one-half of one percent on January 1, 2017 and employees had to then intentionally opt out.

The information was part of the annual report on VRS to the Joint Legislative Audit and Review Commission Monday, covering all aspects of an operation vital to 700,000 participants or beneficiaries. JLARC was presented with a brief oversight, a longer and more detailed overview, and the report of an outside actuary.

Since that first “automatic escalation” the participation has been dropping and it may continue to drop until a second auto-escalation is planned for 2020. “Current low rates of voluntary contribution by hybrid plan members will result in lower retirement income,” the presentation slide states. That’s a major understatement, but the hybrid plan and the low participation are saving the taxpayers a bundle in the short run and will save even more as the previous defined benefits plans fade away.

As of March 1, the overall year to date return was 9.9 percent, slightly behind the goal of 10.0. No figure was given for the end of the fiscal year on June 30 and the last 90 days have been a trade fear-induced roller coaster. The long-term return baked into VRS funding assumptions is 7 percent. The five-year average has been 8.1 percent and the 25-year average 8.2, but as the saying goes, past results are not a guarantee.

The charts tracking the funding status of the various individual retirement plans were all inching up and the average overall is now about 77 percent. Under current assumptions it will take 26 more years to get back to 100 percent funded, where the state was as recently as 2002. The key phrase there is “current assumptions.”

“VRS is actuarially sound” concluded Lance Weiss of Gabriel, Roeder, Smith and Co. (GRS), the outside auditor. He praised Virginia for setting that 7 percent target return a few years back, but then reported it is no longer a conservative assumption but merely a reasonable one. Many of their clients are moving to 6.75 percent, he said. A figure below 6.5 percent was hinted at. With an aging workforce looking at starting benefits in the short term, there is even more reason for Virginia to rethink that 7 percent assumption on return.

The assumption on return is what drives the size of employer contributions. In another report it was noted that if the two largest funds, those for teachers and for general state employees, moved to a 6.75 percent “discount rate” the state would need to increase its annual contribution by $182 million. Changing that assumption also drives up the unfunded liability on both funds and pushes the 100 percent funded goal further out.

The reports today were merely accepted, with few hard (or easy) questions. It may take a longer period of market uneasiness to undermine the current return assumptions, but House Appropriations Chairman S. Chris Jones told reporters after the meeting he would consider it.

Senate Finance Co-Chair Thomas Norment did ask out loud if the hybrid plan was “worth keeping” but the question received no response. The defined benefit plan is gone and unless participation patterns change future VRS retirees (86 percent of whom remain in Virginia) will not have the same comfortable income as current retirees.