by James A. Bacon

Governor Terry McAuliffe announced Thursday that Virginia faces a budget shortfall of roughly $1.5 billion in the current biennial budget. That’s a big short-term problem, one of the worst in recent Virginia history — and possibly the worst ever during a period of economic expansion.

However, the long-term picture doesn’t look any better. The prime culprit is unfunded liabilities in an era of chronic low interest rates.

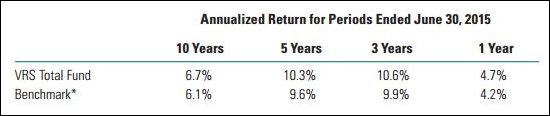

The official actuarial estimate is that the Virginia Retirement System faces a liability of $22.6 billion. As I have noted on many an occasion recently, that assumes that the VRS manages to generate an average 7% return on its $68 billion investment portfolio for the indefinite future. A year ago that didn’t look like such an outrageous proposition. Here’s what VRS’s portfolio performance looked like compared to national benchmarks:

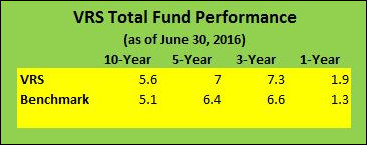

Here’s what the VRS’s most recent (June 2016) comparisons look like:

What a difference a year makes. The average 10-year return is significantly below the assumed 7% figure. The five- and three-year returns do look better, but are they a better representation of likely long-term performance than the 10-year average?

The answer largely depends on which base year we choose to make our comparisons. The three- and five-year comparisons cover periods that were pure bull markets for stocks and bonds. The base year for the 10-year comparison was 2006… just before the Great Recession… thus including a major bear market correction as well as the subsequent bull market. I would argue that the 10-year comparison is more useful because it measures performance from the peak of the early-2ooos business cycle to the peak (or near-peak) of the current business cycle.

If we accept that logic, VRS is not achieving the portfolio growth it needs to meet its own 7% return-on-investment standard. While we can applaud VRS for out-performing its peer pension funds, we should not delude ourselves that 7% growth is a reasonable assumption. In all likelihood, VRS will fall short, and Virginia taxpayers will be called upon to make up the difference.

Perhaps my view is excessively pessimistic, but it is not implausible. The very least we can do is to conduct a sensitivity analysis. If VRS returns are only 5.6% over the next 10 years, then unfunded liabilities will increase to what level? $40 billion? $50 billion? We need to know our potential exposure should things not work out as we hope. It’s better to know this now, when we can plan for it, than get bushwacked by reality a decade from now.