by James A. Bacon

House Speaker William J. Howell is rightfully concerned about the long-term health of the Virginia Retirement System. The pension system’s own actuary estimated a year ago that the $68 billion retirement system has unfunded liabilities of $22.6 billion.

On Sunday, the Richmond Times-Dispatch’s Michael Martz described the debate over restructuring the VRS from a defined-benefits system to a defined-contribution system. Today, Martz reports how Howell is questioning the outsized fees paid to outside fund managers, who handle two-thirds of the system’s assets.

“My biggest concern is the unfunded liability and the fact that it’s just going to grow,” Howell said.

Howell has every reason to be concerned. Unfunded liabilities might turn out to be far bigger than the actuary’s estimate. As I have observed many times, the liability is based upon an assumed 7% annual rate of return on the $68 billion portfolio. If the system under-performs expectations, as the VRS has done the past two years, the unfunded liability can grow by tens of billions of dollars. Writes Martz:

For Howell and other lawmakers on the [Virginia Commission on Retirement Security & Pension Reform], however, the retirement system’s recent investment performance has raised questions about whether the 7% assumed rate of return is too optimistic for the longer term, especially with interest rates keeping bond yields low for the foreseeable future. …

The 7 percent return, lowered by the VRS board from 7.5 percent in 2010 is among the lowest in the country for public pension funds, said Katie Selenski, state policy director for the Pew retirement initiative. “At 7 percent, you’re in a good, prudent position.”

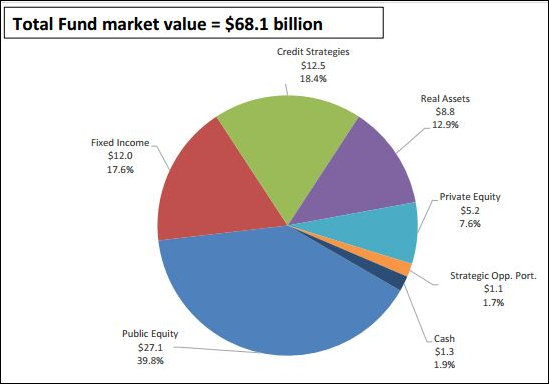

Prudent? Not really. The pie chart above shows VRS’s portfolio allocation. Some 17.6% consists of fixed income assets. Barring some bizarre experiment with negative interest rates in the U.S., there is no way in a zero interest-rate environment that these assets can generate a 7% return. Another 39.8% of the portfolio consists of equities. Insofar as the bull market in stocks over the past 30 years has been driven by lower interest rates and an expansion of earnings multiples, there is no way to replicate the stock gains of the past ten years. Indeed, earnings and earnings quality of stocks are deteriorating, not a good sign for near-term price performance. Meanwhile, the performance of hedge funds nationally has been dismal of late. There is no rabbit to pull out of the magic hat of alternative investments.

For another view on the outlook for long-term portfolio performance, it is instructive to turn to the University of Virginia, which, whatever one might say about the Board of Visitors’ strategic priorities, one must credit with doing an excellent job of managing its endowment. The 10-year return of the University of Virginia Investment Management Company (UVIMCO) has been 10.1 %, according to its 2014-2015 annual report. That compares to 5.8% ten-year performance calculated by the VRS in 2014-2105.

How much do UVa’s masters of the universe think they can earn on their portfolio looking forward? As best as I can tell from perusing UVIMCO’s annual report, they don’t say. UVIMCO doesn’t report that assumption because it isn’t relevant: Although UVIMCO does have unfunded commitments, it is not a pension fund in which shortfalls must be made up by taxpayers.

Still, it is possible to get a sense of UVa’s expectations from comments made by university officials that they expect the controversial $2.2 billion Strategic Investment Fund to throw off $100 million a year to pay for programs to advance the university’s strategic goals. University officials have not explained what rate-of-return assumptions they are using. But a simple calculation reveals that $100 million is only 4.5% of $2.2 billion.

From that, one can draw one of two conclusions. Either UVa’s investment mavens are assuming a much lower rate of return than the VRS, or they expect a higher-than-4.5% rate of return but plan to retain a substantial fraction of the earnings, presumably in order to grow the size of the portfolio.

It appears that the second conclusion is true. Here’s what the UVIMCO annual report says: “Each year a portion of the endowment value is paid out to support the fund’s purpose, and any earnings in excess of this distribution help build the fund’s market value over time. In this way, an endowment fund grows and provides support for its designated purpose in perpetuity.”

For legislators digging into UVa’s controversial Strategic Investment Fund, which is managed by UVIMCO, it would be interesting to know what rate-of-return the university is assuming for its endowment and what percentage it figures on spending and what percentage it figures on retaining. The numbers should be equally interesting to Speaker Howell. It would send out a flashing yellow caution signal if the UVIMCO’s assumption about of future performance was more conservative than that of the VRS.