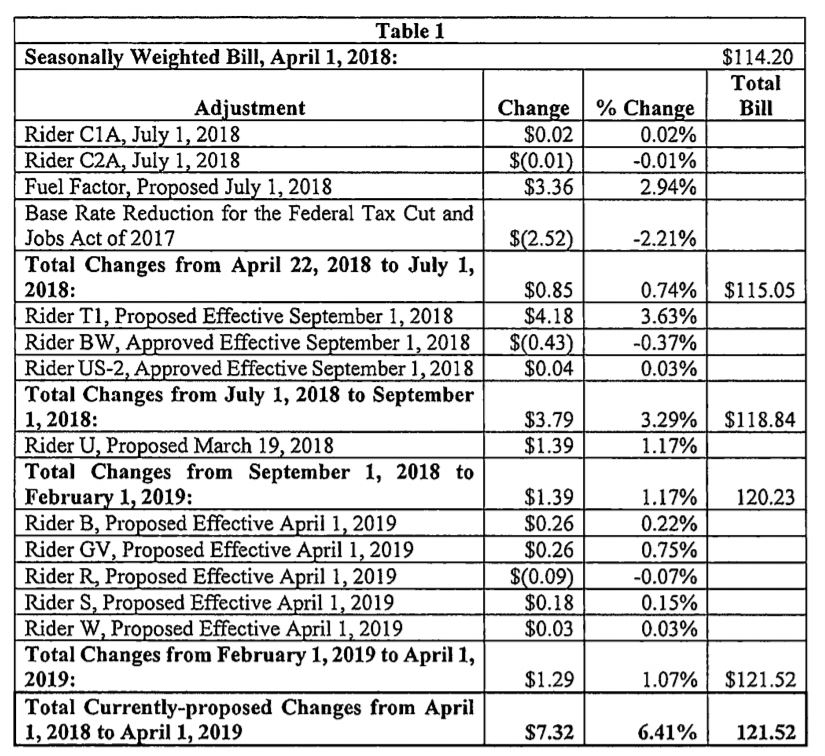

Net impact of pending Dominion rate adjustments on a residential bill for 1000 kwh. Source: SCC Staff

A recently-filed estimate by the State Corporation Commission staff projects that a typical residential bill for a Dominion Energy Virginia customer will rise more than $7, or more than 6 percent, by next April, despite expected adjustments in the customers’ favor due to the Tax Cuts and Jobs Act (TCJA) of 2017.

The utility is seeking to retain a $71 million portion of that tax reduction windfall until at least September 1, 2019 – a full 20 months after Congress cut the taxes and almost 18 months after the General Assembly confirmed that the tax cuts should flow through to customers.

A chart filed with testimony by David J. Dalton of the SCC staff, reproduced above, tracks 13 specific adjustments to the complicated billing process either approved by the SCC or pending. Each of the riders listed is for a specific generation facility or cost, such as the separate charge for fuel which is adjusted annually and this year is expected to rise. You can find a brief explanation of each here.

The testimony dealt with one of the larger upward adjustments, a separate rider charge for regional transmission services designated as Rider T1. Arguments over that rider are set for Friday morning in front of an SCC hearing examiner. As proposed it would add more than $4 a month to that 1000 kwh bill.

As part of the regional transmission organization PJM Dominion pays that entity for transmission services and then passes the costs directly to customers. For 2018 Dominion is seeking to recover $755.5 million from customers, which is more than 20 percent higher than the amount approved in the 2017 annual review.

Like most of the matters before the SCC, a large record has already been built and in general the SCC staff agrees with the utility’s accounting and request. There are two major points of disagreement, the largest of which involves the taxes. Dominion made no reduction to its request even though it includes about $71 million more for 2018 taxes than may be paid, claiming Congress acted too late in 2017 to change it.

One element of a complicated 2018 state law on electricity regulation directed the state’s major electric utilities to quickly adjust their bills to reflect the lower federal taxes, which are included in base rates as a pass-through cost. You can also see the impact of that coming change on the SCC chart above, which includes a $2.52 reduction for the lower taxes.

The legislation directed the return of taxes included in rates for “generation and distribution” but did not mention transmission. It made no specific mention of taxes paid by PJM and then charged to the utility and passed on to its customers. The state’s other major utility, Appalachian Power Company, has made the tax adjustment in its request for the 2018 transmission rider approval.

Making that adjustment would cut Dominion’s request for additional Rider T1 revenue – and the resulting monthly increase to customers – by more than half. The $71 million in question would increase the tax cut’s benefit to customers another 57 percent over the $125 million reduction in the legislation.

In company testimony Dominion pushed back and argues that there will ultimately be no harm to consumers as it will all come out in the wash in the 2019 Rider T1 review. The SCC’s Patrick W. Carr writes that fixing it now will “minimize future over-recoveries that will result from a revenue requirement in this case that ignores the TCJA’s effects.”

The other dispute involves less than $13 million. Because Dominion is being forced by PJM to keep its Yorktown generation facility open longer than planned, awaiting construction of a delayed power line, PJM is paying Dominion $13 million to cover the cost of operating the plant.

The SCC staff is arguing that money should be a credit on the Rider T1 transmission revenue requirement because PJM collects it as a transmission cost before paying Dominion. If fact, Dominion is paying about $5 million to PJM toward that $13 million cost and collecting it under this rider. (The rest is coming from other load-serving entities on PJM). Dominion is arguing the revenue belongs to its generation unit and should not reduce its need for T1 revenue.

Whether the money belongs in the rider or base rates matters because Dominion’s base rates remain frozen until at least 2022 so if the additional revenue is profit the company will keep it. This illustrates the benefit to the utility of having its base rates protected from adjustment, while at the same time having near certainty that costs in other areas can and will be passed on to customers. Expect similar skirmishes in coming years over the murky border between riders and base rates.